Before learning what you can deduct, you must understand what you cannot deduct.

🚫 Non-Deductible Expenses

Expense

Why Not Allowed

Commuting to work

Considered personal travel

Business clothing

Personal clothing

Haircuts or grooming

Personal expense

Gym memberships

Personal benefit

Meals during regular workday

Personal consumption

⚠️ Key Rule

If an expense is personal in nature, it cannot be deducted — even if it helps you perform your job better.

2️⃣ Who Can Claim Employment Expenses (Eligibility Rules)

Not every employee qualifies to deduct work expenses.

✅ You can claim employment expenses if:

Your employment contract requires you to pay for certain expenses

Your employer does not reimburse you

You have a signed T2200 form

Example

Situation

Deductible?

Using your own vehicle for work travel

✅ Yes

Driving to your regular office

❌ No

Receiving non-taxable vehicle allowance

❌ No

3️⃣ The T2200 Form – Declaration of Conditions of Employment

The T2200 form is one of the most important documents when claiming employment expenses.

📄 Purpose of T2200

It confirms:

The employee must pay certain expenses

Whether the employee travels for work

If the employee receives allowances or reimbursements

If the employee works from home

⚠️ Important

Rule

Explanation

Employer must complete the form

Employees cannot create it

Must be signed

Unsigned forms are invalid

Not filed with return

Keep it for CRA review

4️⃣ The T777 Form – Statement of Employment Expenses

Once eligibility is confirmed using T2200, expenses are calculated on Form T777.

🧾 Purpose

The T777 lists all deductible expenses such as:

Vehicle expenses

Home office expenses

Office supplies

Work phone costs

Advertising (for commission employees)

Flow of Forms

Form

Purpose

T2200

Confirms eligibility

T777

Calculates expenses

T1 Return

Reports deduction

5️⃣ Framework for Deducting Employment Expenses

Claiming employment expenses follows a clear process.

Step-by-Step Framework

1️⃣ Obtain signed T2200 2️⃣ Review allowed expenses 3️⃣ Collect receipts and records 4️⃣ Complete T777 5️⃣ Apply employment-use percentages 6️⃣ Exclude reimbursements 7️⃣ Enter deduction on Line 22900

6️⃣ Example: Vehicle Expense Deduction

Vehicle expenses are one of the most common employment deductions.

Example Scenario

Jason uses his personal truck for work.

Expense

Amount

Fuel

$6,000

Repairs

$2,500

Insurance

$2,200

Lease payments

$6,500

Other costs

$544

Total

$17,744

If 66% of driving is for work:

$17,744 × 66% = $11,771 deductible

7️⃣ Two Types of Vehicle Allowances

Employers may compensate employees for vehicle use in two ways.

🚗 Vehicle Allowance Types

Type

Tax Treatment

Flat monthly allowance

Taxable

Per-kilometre reimbursement

Usually non-taxable

Understanding this difference is essential for correct deductions.

8️⃣ When a Flat Vehicle Allowance Is Received

A flat allowance (example: $600/month) is always taxable.

How It Works

1️⃣ Allowance appears on the T4 slip 2️⃣ It increases employment income 3️⃣ Employee can claim actual vehicle expenses

9️⃣ When a Per-Kilometre Allowance Is Received

If the employer reimburses based on actual kilometres driven, the payment may be non-taxable.

Example

Jason drives 19,185 km for work.

Allowance:

19,185 × $0.46 = $8,825

Because the rate is reasonable:

Not included on T4

No tax payable

🔟 When Reimbursement Does Not Cover All Costs

Sometimes reimbursement is less than actual expenses.

Two Ways to Handle It

Method

Explanation

Add reimbursement to income

Deduct full expenses

Subtract reimbursement

Deduct only the difference

Both methods lead to the same result.

1️⃣1️⃣ Home Office Expenses – What Can Be Claimed

Employees working from home may deduct certain expenses.

Eligible Expenses

Expense

Deductible

Electricity

✅

Heating

✅

Water

✅

Internet (monthly fees)

✅

Rent (if renting)

✅

Commission employees may also claim:

Home insurance

Property taxes

1️⃣2️⃣ Home Office Expense Example

Example:

Expense

Annual Amount

Rent

$18,000

Utilities

$2,400

Internet

$600

Workspace = 10% of home

Deduction:

Expense

Deductible

Rent

$1,800

Utilities

$240

Internet

$60

Total deduction = $2,100

1️⃣3️⃣ Example of Other Employment Expenses

Employees may also claim work-related costs such as:

Parking

Office supplies

Cell phone usage

Postage

Small maintenance items

Example:

Expense

Amount

Cell phone

$750

Parking

$400

Supplies

$466

Total = $1,616

1️⃣4️⃣ Example with Reimbursed Expenses

If the employer reimburses certain expenses:

❌ Those expenses cannot be deducted.

Example:

Expense

Reimbursed

Deductible

Parking

Yes

❌

Office supplies

Yes

❌

Vehicle allowance

Taxable

✅

1️⃣5️⃣ Special Rules for Commission Employees

Employees paid by commission have additional deductions available.

They may claim:

Advertising expenses

Promotion costs

Property taxes (home office)

Home insurance

Certain travel expenses

But they must:

Earn commission income

Have T2200 confirming eligibility

1️⃣6️⃣ Example: Commission Employee Expenses

Example commission salesperson deductions:

Expense

Amount

Vehicle costs

$6,200

Advertising

$1,200

Home office

$1,400

Total employment expenses = $8,800

1️⃣7️⃣ Additional Expenses That Cannot Be Deducted

Even if work-related, some expenses remain non-deductible.

Examples include:

Mortgage payments

Furniture

Home renovations

Decorations

Personal phone usage

These are considered capital or personal expenses.

1️⃣8️⃣ Filing Requirements for Employment Expenses

When filing taxes with employment expenses:

Documents Required

Document

Purpose

T2200

Confirms eligibility

T777

Calculates deduction

Receipts

Proof of expenses

Mileage log

Proof of vehicle usage

⚠️ CRA may request these during a review.

1️⃣9️⃣ CRA Guide T4044

For full details on employment expenses, the CRA provides Guide T4044 – Employment Expenses.

This guide explains:

deductible expenses

eligibility rules

documentation requirements

examples for different professions

✅ Quick Recap – Deducting Employment Expenses

To claim employment expenses correctly:

✔ Get a signed T2200 from your employer ✔ Track expenses and keep receipts ✔ Separate personal vs employment use ✔ Calculate deductions using T777 ✔ Report total on Line 22900 of the T1

⭐ Final Tip for New Tax Preparers

Employment expenses are one of the most frequently reviewed deductions by the CRA.

Always verify:

Eligibility

Documentation

Accurate calculations

This helps ensure returns are accurate, compliant, and audit-proof.

When preparing Canadian tax returns, employment income is usually the foundation of the entire return. Understanding how it is reported, what slips are used, and which deductions or credits apply will help you prepare accurate returns and avoid CRA reassessments.

This guide summarizes the essential concepts every tax preparer should know.

1️⃣ 🧾 Introduction to Employment Income & Employment Expenses

Employment income refers to money or benefits received from working for an employer. It is one of the most common types of income reported on Canadian tax returns.

💰 What Counts as Employment Income

Typical examples include:

Salary or wages

Bonuses and commissions

Overtime pay

Vacation pay

Tips or gratuities

Taxable benefits from employers

📄 Most of this income is reported on a T4 slip (Statement of Remuneration Paid).

💸 What Are Employment Expenses?

Certain employees may deduct work-related expenses paid out of pocket, such as:

Vehicle expenses for work

Work supplies or tools

Home office expenses

Work-related phone or internet

Meals or lodging (specific professions)

⚠️ Important rule:

You can only claim employment expenses if your employer signs Form T2200 – Declaration of Conditions of Employment.

🔎 CRA Review Risk

Because employment expenses are often misused:

CRA may request receipts

Claims can be audited

Incorrect claims may lead to reassessment

✅ Best practice: keep receipts, logs, and supporting documents.

2️⃣ 💼 Employment Income – What Is Included

Employment income includes all money and benefits received because of employment.

Common Types of Employment Income

Type

Examples

Regular Pay

Salary, wages, commissions

Extra Pay

Overtime, bonuses

Leave Pay

Vacation pay

Exit Payments

Severance or retiring allowances

Employer Benefits

Company car, insurance premiums

Employer Contributions

RRSP contributions, stock options

💡 Good to know:

Employers calculate taxable benefits and include them on the T4 slip, so preparers normally do not calculate them manually.

3️⃣ 📝 Recording Employment Income on the T4 & T1

The T4 slip acts as a map for entering employment income into the T1 personal tax return.

Important T4 Boxes

T4 Box

Meaning

T1 Line

Box 14

Employment income

Line 10100

Box 16

CPP contributions

Tax credit

Box 18

EI premiums

Tax credit

Box 24

EI insurable earnings

Info only

Box 26

CPP pensionable earnings

Info only

Box 40

Taxable benefits

Included in Box 14

Union dues

Payroll deduction

Line 21200

Key Tips for Preparers

✔ Enter each T4 slip separately ✔ Verify every box on the slip ✔ Some boxes affect deductions or credits

⚠️ Mistakes in T4 entries can trigger CRA reassessments.

4️⃣ ⚠️ Common T4 Errors to Watch For

Even experienced preparers sometimes miss important details on a T4.

Most Common Mistakes

❌ Only entering Box 14 ❌ Missing deductions in lower sections ❌ Forgetting union dues or donations ❌ Ignoring health plan premiums ❌ Assuming everything is included in Box 14

Boxes That Often Get Missed

Box

Item

Impact

67

Severance / retiring allowance

Line 13000

85

Health plan premiums

Medical credit

Union dues

Payroll deduction

Line 21200

Payroll donations

Charitable credit

Schedule 9

✅ Pro Tip

Always review every box on the T4 — not just the top section.

5️⃣ 📄 Employment Amounts on T4A and T4PS Slips

Besides the T4, some employment-related income appears on other slips.

🟢 T4A Slip – Other Employment Income

Common items:

Research grants

Wage-loss replacement benefits

Medical benefits for former employees

Other special employment payments

📍 Usually reported on Line 10400 – Other Employment Income

🟢 T4PS Slip – Profit Sharing

Used when employees receive dividends from company profit-sharing plans.

Important facts:

Treated as dividend income

Reported on dividend lines of the T1

Dividends are grossed up before calculating taxable income

6️⃣ 💼 Casual Labour, Tips & Odd Jobs (No Slip)

Sometimes clients earn income without receiving a tax slip.

Examples:

Temporary labour

Babysitting

Tutoring

Cash tips

Small contract work

⚠️ CRA rule:

All income must be reported even if no slip was issued.

📍 Typically reported on Line 10400.

Good Practice

Encourage clients to keep:

Payment records

Logs of work performed

Tip tracking records

7️⃣ 💼 Reporting Tips & Casual Income on the T1

🍽 Tips and Gratuities

Tips are fully taxable, whether:

Cash tips

Electronic tips

Shared tip pools

📍 Report on Line 10400 – Other Employment Income

⚠️ Preparers should never estimate tips — use client records only.

🔧 Casual Work & Odd Jobs

Situation

How It Is Reported

Single employer

Employment income (Line 10400)

Multiple clients

Business income

If classified as business income, the client may deduct expenses such as:

Vehicle costs

Advertising

Phone expenses

8️⃣ 💼 Wage-Loss Replacement Plan Income

Wage-loss replacement plans provide income when employees cannot work due to illness or injury.

Examples include:

Disability benefits

Workplace injury insurance

Employer insurance plans

How It Is Reported

Source

Slip

Employer paid

T4

Insurance company

T4A

Taxable Amount

Only the portion not funded by employee contributions is taxable.

Example:

Item

Amount

Benefit received

$24,000

Employee contributions

$4,800

Taxable income

$19,200

9️⃣ 📊 CPP & EI Premiums and Tax Credits

Most employees contribute to two national programs:

Program

Purpose

CPP

Retirement income

EI

Temporary unemployment benefits

Where They Appear on T4

Box

Contribution

Box 16

CPP

Box 18

EI

Tax Return Credits

Credit

T1 Line

CPP

Line 30800

EI

Line 31200

💡 Since 2019, enhanced CPP contributions also create a small deduction (Line 22215).

Maximum Contribution Limits

Each year the government sets limits.

Once earnings exceed the limit:

CPP deductions stop

EI deductions stop

This means high-income workers still pay the same maximum as others above the threshold.

🔟 Schedule 8 & T2204 – CPP and EI Overpayments

Employees with multiple jobs often overpay CPP or EI.

Why?

Each employer deducts contributions independently.

Example

Job

Income

CPP

EI

Job 1

$60,000

$2,898

$856

Job 2

$18,700

$800

$296

Total CPP = $3,698 → Overpayment

How the Refund Works

Form

Purpose

Schedule 8

Calculates CPP contributions

T2204

Calculates EI overpayments

Refund Lines

Refund

T1 Line

CPP overpayment

Line 44800

EI overpayment

Line 45000

💰 Overpayments are refunded automatically when the tax return is filed.

✅ Quick Recap for Tax Preparers

✔ T4 slips report most employment income ✔ Other slips include T4A and T4PS ✔ Tips and cash income must still be reported ✔ CPP and EI contributions generate tax credits ✔ Multiple jobs may create refundable overpayments ✔ Schedule 8 and T2204 handle those refunds

⭐ Final Tip

The best tax preparers don’t just enter numbers — they understand where each amount comes from and why it appears on the tax return.

🧾 1️⃣ Employment Income: What It Really Means for You

Employment income is everything you earn from working for someone else.

That includes:

Salary or hourly wages

Overtime

Bonuses

Vacation pay

Tips

Some employer-paid benefits

Most of this appears on your T4 slip.

💡 Why this matters: Your employment income determines:

How much tax you owe

What credits you qualify for

Whether you get a refund

The higher your income, the more important it becomes to claim every eligible deduction and credit.

📄 2️⃣ Your T4 Slip: Don’t Just Look at Box 14

Most people only look at:

Box 14 – Employment Income

But that’s a mistake.

Your T4 contains several refund-boosting items.

Here’s what you should look for:

T4 Box

What It Means

How It Can Increase Your Refund

Box 16

CPP Contributions

Creates a tax credit

Box 18

EI Premiums

Creates a tax credit

Union Dues

Money paid to union

Deductible expense

Box 85

Health plan premiums

Eligible for medical credit

Box 67

Retiring allowance

Special reporting (may allow tax planning)

✨ Refund Tip: Union dues and private health plan premiums are commonly missed — and they directly increase your refund.

⚠️ 3️⃣ The Most Common T4 Mistakes That Cost People Money

Many people:

Ignore the bottom half of the T4

Miss union dues

Forget payroll donations

Overlook private health premiums

Miss retiring allowances

Even small missed amounts can reduce your refund.

Example:

Emma paid $1,200 in union dues. If she forgets to claim it, she loses hundreds in potential refund.

📌 Small detail. Real money.

💰 4️⃣ Worked More Than One Job? You Might Get CPP & EI Money Back

This is one of the biggest hidden refund boosters.

Canada sets yearly maximums for:

CPP (Canada Pension Plan)

EI (Employment Insurance)

If you worked two or more jobs:

Each employer deducted CPP and EI separately.

You may have overpaid.

Good news:

✔ The CRA automatically refunds the excess. ✔ It increases your refund directly. ✔ It’s dollar-for-dollar.

Example:

If you overpaid $600 in CPP and $250 in EI, Your refund increases by $850.

Many people don’t even realize this is happening.

💼 5️⃣ T4A & T4PS Slips: Income You Might Not Understand

🟢 T4A – Other Employment Income

This may include:

Wage-loss replacement benefits

Disability payments

Research grants

These are taxable.

But here’s the key 👇

If you contributed to the insurance plan yourself, your contributions reduce the taxable amount.

If you don’t deduct your contributions, you could overpay tax.

🟢 T4PS – Profit Sharing (Dividends)

This is different from salary.

It’s dividend income.

And dividends receive a special tax credit.

💡 This can reduce the tax you owe.

💵 6️⃣ Tips, Side Jobs & Cash Income (Yes, It Must Be Reported)

If you earned:

Cash tips

Babysitting income

Freelance or odd jobs

Cash payments without a T4

You must report it.

But here’s where refund strategy comes in 👇

One employer?

→ Report as employment income.

Multiple clients?

→ Report as business income.

Why does this matter?

Because business income allows you to deduct expenses.

📊 Example: How Classification Changes Your Refund

Sarah babysits for 5 families and earns $6,000.

If she reports it as employment income:

She pays tax on full $6,000.

If she reports it correctly as business income: She may deduct:

$800 vehicle use

$300 supplies

$200 phone use

Now she pays tax on only $4,700.

That reduces taxable income and increases her refund.

📌 Correct classification = real savings.

🏥 7️⃣ Wage-Loss or Disability Benefits: Avoid Overpaying Tax

If you received wage-loss replacement benefits:

They are taxable.

But if you paid into the plan (through payroll deductions), those contributions reduce what’s taxable.

Example:

You received $20,000 in benefits. You contributed $4,000 to the plan.

Taxable amount = $16,000.

If you forget the contribution deduction, you overpay tax on $4,000.

That could cost you hundreds.

🏠 8️⃣ Employment Expenses: The Big Refund Opportunity (If You Qualify)

Most employees cannot deduct work expenses.

But you may qualify if:

Your employer required you to pay work expenses

You were not reimbursed

You have a signed T2200 form

Eligible expenses may include:

Vehicle use for work

Home office expenses

Tools and supplies

Cell phone (work portion)

Internet (work portion)

⚠ CRA reviews these claims carefully.

But if legitimate, they can significantly reduce taxable income.

Example:

Jason earns $75,000. He qualifies for $4,000 in employment expenses.

Now he’s taxed on $71,000 instead.

That could increase his refund by over $1,000.

🧮 9️⃣ CPP & EI Credits: How They Reduce Your Tax

CPP and EI aren’t just deductions from your paycheck.

They create tax credits.

CPP → reduces federal tax

EI → reduces federal tax

There are annual maximums.

If you exceed them, you get refunded.

Also:

Since 2019, enhanced CPP contributions include:

A tax credit portion

A deduction portion

Tax software usually calculates this automatically — but it’s good to understand why your refund increases.

📑 🔟 Schedule 8 & T2204: The Hidden Refund Forms

If you worked multiple jobs:

Schedule 8 calculates CPP overpayment. T2204 calculates EI overpayment.

You don’t need to manually calculate these — but entering all T4 slips properly ensures:

✔ The refund happens ✔ You don’t leave money behind

🚨 The Top 10 Ways People Lose Refund Money

Forgetting a T4

Missing union dues

Ignoring medical premiums

Misclassifying side income

Not deducting wage-loss contributions

Forgetting business expenses

Not checking CPP/EI overpayment

Ignoring lower T4 boxes

Guessing tip amounts

Claiming expenses without documentation

🏆 Final Refund Maximization Checklist

Before filing, ask yourself:

✔ Did I enter every T4? ✔ Did I check every box? ✔ Did I claim union dues? ✔ Did I include medical premiums? ✔ Did I report tips properly? ✔ Did I classify side income correctly? ✔ Did I deduct insurance contributions? ✔ Did I check CPP/EI overpayment? ✔ Do I qualify for employment expenses?

If you answered “no” to even one — you might be leaving money behind.

💡 Final Thought

Maximizing your refund isn’t about aggressive tactics.

It’s about:

Understanding what reduces taxable income

Claiming eligible credits

Avoiding small mistakes

Paying attention to detail

Most refunds are won or lost in the fine print — not the headline numbers.

Whether you are learning to become a tax preparer or you simply want to file your own return using Intuit ProFile, this guide will show you—step by step—how a basic Canadian tax return is actually prepared.

We will use a typical real-life style example:

One T4 employment slip

RRSP contributions

Medical expenses

Charitable donations

No business income and no dependants

This is exactly the kind of client a new tax preparer will see every day—and it’s also the perfect situation for someone filing their own taxes for the first time.

1. Start With the Documents – Tax Preparation Is 90% Organization

Before opening any software, collect the paperwork. Good tax habits start here.

For our example client you need:

T4 slip from employer

RRSP receipts

$3,000 for March–December

$600 for January–February (first 60 days)

Notice of Assessment showing RRSP limit $88,700

Dental receipt $3,620

Donation receipts $420

Client facts:

Single, no dependants

Date of birth used for training: 1991-03-05

Employment income: $78,500

💡 Tip for new preparers: Always ask for the Notice of Assessment. Without the RRSP limit you can accidentally create an over-contribution.

2. Create the File in Intuit ProFile

Open Intuit ProFile T1 and choose:

New → T1 Return

Enter the identification:

Name and SIN

Address

Date of birth

Marital status: Single

For people filing their own return, this screen is simply your personal profile. For future tax preparers, this is where accuracy is critical—one wrong SIN can reject an entire filing.

3. Enter the T4 Slip – The Heart of Most Returns

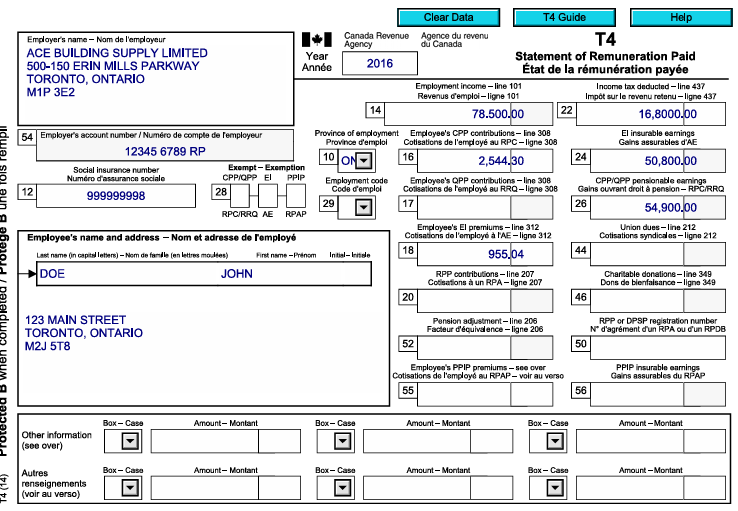

Open the T4 entry screen and type the main boxes exactly as shown on the slip:

Box 14 – Employment income: 78,500

Box 16 – CPP: 2,544.30 (Tax software will show the correct value; based on CRA formula)

Box 18 – EI: 955.04 (Tax software will show the correct value; based on CRA formula)

Box 22 – Tax deducted: 16,800

Let ProFile calculate the rest.

Professional Tip: Do not override CPP/EI insurable earnings unless you truly know why. The software follows CRA rules automatically.

After saving, check the T1 Summary:

Employment income appears on line 10100

CPP & EI credits are created

Canada Employment Amount shows automatically

This single step builds most of the return.

4. RRSP Contributions – Where Many Beginners Make Mistakes

Step 1 – Enter the RRSP Limit First

Go to the RRSP section and enter:

Limit from NOA: $88,700

If you skip this, ProFile assumes zero room and will refuse the deduction.

Step 2 – Enter the Receipts

On Schedule 7 record:

$3,000 (Mar–Dec)

$600 (Jan–Feb)

Total deduction = $3,600

Now line 20800 of the return shows the RRSP claim.

For self-filers: this is how you legally reduce your taxable income. For preparers: this is one of the biggest refund drivers.

5. Medical Expenses – Use the Worksheet

Open Medical Expenses Worksheet:

Patient: John

Type: Dental

Amount: $3,620

ProFile automatically applies the CRA rule:

Medical expenses – lesser of • 3% of income • CRA minimum threshold

The allowable amount flows to Schedule 1 without you doing math.

6. Charitable Donations

Open the Donations Worksheet:

United Way – $300

Make-A-Wish – $120

Total = $420

The software calculates:

First $200 at lower credit rate

Balance at higher rate

For new preparers: never add donations directly on the T1—always use the worksheet so carry-forwards are tracked.

7. Review the Result

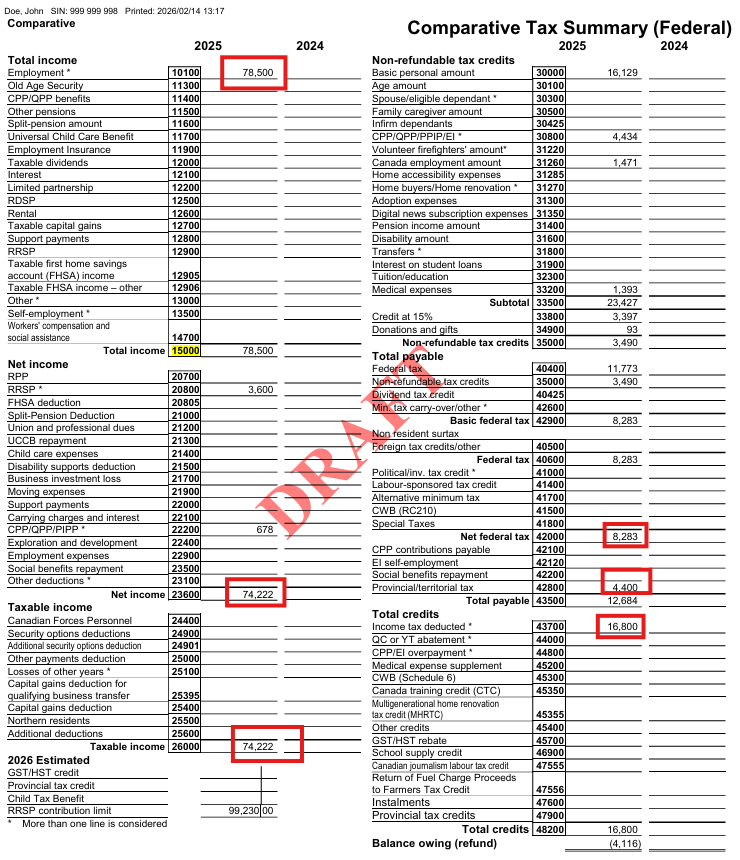

Open the Comparative Summary:

You should see:

Total income: $78,500

Net income after RRSP: $74,900

Credits for CPP, EI, employment amount

Medical and donations applied

➡ Refund: $1,543.16

This is the moment both preparers and self-filers love 😊.

8. Check Next Year RRSP Room

The RRSP worksheet shows:

New contribution limit: $99,230

A good preparer will always tell the client this number. A self-filer should keep it for next year’s planning.

9. Quality Check – Think Like a Professional

Before hitting EFILE:

Is the DOB correct?

RRSP limit entered?

Receipts listed properly?

Marital status accurate?

No duplicate entries?

Tax preparation is less about typing and more about reviewing like an auditor.

10. What This Teaches You

If You Are Training to Be a Tax Preparer

You just practiced:

Reading a T4 slip

Claiming RRSP correctly

Calculating medical credits

Entering donations

Navigating ProFile screens

Explaining results to a client

This is the foundation for 70% of real clients.

If You Are Filing for Yourself

You learned:

Where your refund actually comes from

How RRSP lowers tax

Why medical and donations matter

How ProFile mirrors CRA forms

Summary Review — Understanding the Forms ProFile Generated

At this point you have already entered the slips and receipts in Intuit ProFile and received a refund result.

But a real tax preparer must understand something deeper:

Where exactly did every number go — and why did the refund happen?

ProFile does not invent numbers. It simply places your entries into the CRA calculation system in a specific order:

Income → Deductions → Net Income → Tax → Credits → Refund

Below is a guided walk-through connecting what you typed to what CRA calculated.

1) Income — Where the Return Begins

You entered one T4 slip:

Employment income = $78,500

That single entry populated:

T1 Line 10100 → Employment income

Total income Line 15000 → 78,500

T1 Summary total income → 78,500

What CRA is doing: Before any planning or deductions, CRA asks:

“How much money did the taxpayer earn?”

Because there are no investments, business, or rental income, total income equals employment income.

2) Deductions — Reducing Taxable Income

Now we move to the first tax-planning stage.

RRSP deduction

$3,600 → Line 20800

CPP enhanced deduction

$678 → Line 22215

Net Income Calculation

Total income: 78,500 Minus deductions: 4,278

Net income = 74,222

Line 23600

This is one of the most important numbers in a tax return. It controls benefits, credits, and thresholds.

3) Taxable Income

There were no additional adjustments.

So:

Taxable income = Net income = 74,222

Line 26000

4) Federal Tax Before Credits

CRA now applies tax brackets to taxable income.

Result:

Federal tax = 11,773

This is the tax owed before applying credits.

5) Non-Refundable Credits — Reducing the Tax

Credits do NOT reduce income. They directly reduce the tax bill.

Automatic credits from employment

Basic personal amount → Line 30000

CPP contributions → Line 30800

EI contributions → Line 31200

Canada employment amount → Line 31260

Medical expenses (you entered $3,620)

CRA rule: subtract 3% of income

3% of 74,222 = 2,226.66 Eligible medical = 3,620 − 2,226.66 = 1,393.34

Line 33200

Donations (you entered $420)

Credit calculated automatically:

92.80

Total federal credits

3,489.70

6) Final Tax After Credits

Federal tax before credits: 11,773 Minus credits: 3,489

Net federal tax = 8,283

Add Ontario tax:

4,400

Total tax payable = 12,683

7) Refund Calculation — The Real Meaning of a Refund

Tax already deducted by employer (T4 Box 22):

16,800

Actual tax owing:

12,683

Refund:

4,116

8) Next Year RRSP Room

ProFile also calculated next year planning value:

New RRSP limit = 99,230

What These Three Forms Each Teach You

T1 Return The legal CRA calculation — how tax law works.

👨💼 Simple Employee With a T4 Slip – Understanding Employment Income & Key Tax Credits

📌 Starting With the Most Common Tax Situation

For most Canadians, the first tax return you will ever prepare is for an employee who receives a T4 slip. This is the foundation of personal tax preparation, and mastering it will make everything else easier.

A T4 employee return may look simple, but there are many details that can cause errors if you don’t understand:

what each box means

where amounts flow on the T1

which credits the taxpayer receives

how pensions and adjustments affect RRSP room

Let’s break it down step by step.

🧾 What a T4 Slip Tells You

A typical T4 includes:

Employment income (Box 14)

CPP contributions

EI premiums

Income tax deducted

RPP contributions

Pension adjustment

Other taxable benefits (Box 40)

👉 Your job is to transfer this information accurately into tax software and understand the tax effect behind each number.

🧩 Where T4 Amounts Appear on the Tax Return

1️⃣ Employment Income – Line 10100

Box 14 flows directly to employment income

This is the starting point for tax calculations

Includes wages, bonuses, commissions, and most benefits

2️⃣ CPP & EI – Non-Refundable Tax Credits

Employees receive a credit for:

CPP contributions

EI premiums

These appear on Schedule 1 – Federal Tax Credits and reduce tax payable.

3️⃣ Canada Employment Amount 💼

Every employee is eligible for the Canada Employment Credit, up to an annual maximum.

✔ This is automatic ✔ Only available to employees ✔ Helps reduce federal tax

4️⃣ Registered Pension Plan (RPP) Contributions

If the T4 shows RPP deductions:

The employee receives a deduction similar to RRSP

It reduces net income

It also creates a pension adjustment

⚠️ The Pension Adjustment – Why It Matters

The Pension Adjustment (PA) reduces how much RRSP room the person will get next year.

Think of it this way:

The government allows about 18% of earnings for retirement saving. If part is already saved in a work pension, RRSP room must shrink.

This is one of the most misunderstood parts of a T4.

🚨 Common Beginner Mistakes With T4s

❌ 1. Missing Boxes

Many preparers only enter:

Box 14

Tax deducted

But forget:

Box 40 – taxable benefits

RPP amounts

Pension adjustment

Union dues or other boxes

👉 Every box matters!

❌ 2. Overriding Calculated CPP/EI

Tax software automatically calculates:

CPP pensionable earnings

EI insurable earnings

Never override these unless you are 100% certain the T4 is wrong.

👉 Wrong overrides = CRA reassessments.

❌ 3. Ignoring Large Box 40 Amounts

If “Other Taxable Benefits” are high:

🔎 Investigate!

It could mean:

vehicle benefits

allowances

RRSP contributions through work

potential employment expense claims

🧮 How Professionals Review a T4 Return

A good preparer will:

Enter all boxes exactly

Follow the flow to:

Schedule 1

Provincial credits

Net income

Check RRSP limit impact

Ask follow-up questions about:

benefits

allowances

expenses

🗂 Practical Workflow for Beginners

Step 1 – Enter the Slip

Match every box

Don’t assume blanks

Verify names and SIN

Step 2 – Review Credits

CPP credit

EI credit

Canada Employment Amount

Step 3 – Analyze Pension Items

RPP deduction

Pension adjustment

RRSP room impact

Step 4 – Ask the Client

Any employment expenses?

Vehicle use?

RRSP through payroll?

💡 Key Takeaways

✔ A “simple T4” is not always simple ✔ Every box affects a different part of the return ✔ Pension adjustment controls future RRSP room ✔ Box 40 can hide valuable deductions ✔ Never override CPP/EI without proof

💼 Employee With Multiple T4 Slips – CPP & EI Overpayments + Smart Client Advice

🔍 What Happens When a Client Has More Than One Job?

It’s very common for Canadians to work:

a full-time job

plus a part-time or weekend job

or switch employers during the year

When this happens, the tax return becomes a little more interesting—especially for CPP and EI contributions.

👉 Each employer calculates deductions as if they are the only employer. 👉 But CPP and EI have annual maximum limits.

This usually leads to overpayments that must be refunded on the personal tax return.

🧮 Why CPP & EI Overpayments Occur

Let’s break this down in simple terms:

✔ Every worker pays CPP and EI through payroll ✔ There is a maximum yearly contribution ✔ Employers don’t talk to each other ✔ The second employer keeps deducting—even if the max was already reached

Result?

💰 The taxpayer gets money back when filing their T1 return.

📌 Where the Refund Shows on the Return

The tax software (or CRA forms) automatically calculates:

Schedule 8 – CPP overpayment

Form T2204 – EI overpayment

These amounts appear on the T1 as:

Line 44800 – CPP overpayment refund

Line 45000 – EI overpayment refund

👉 This becomes part of the client’s refund or reduces their balance owing.

⚠️ The BIG Surprise for Clients

Here’s the part many beginners don’t expect:

Even though the client gets CPP & EI back, they may still…

🚨 OWE TAX at the end of the year!

Why?

Because each employer withholds income tax based only on their own payroll, not the client’s total income.

📘 Example of the Real-World Problem

Imagine:

Job #1 pays $135,000

Job #2 pays $14,000

Employer #2 withholds tax as if the person only earns $14,000.

But CRA taxes the client on:

👉 $149,000 TOTAL income

This pushes the client into a higher tax bracket, creating a balance owing.

🗣 How to Advise Your Client

This is where you become more than a data entry person—you become an advisor.

You should explain:

“Your second employer didn’t know about your first job, so not enough tax was withheld.”

🛠 Practical Solutions You Can Suggest

Option 1 – Adjust Payroll Withholdings

The client can update their TD1 form with the employer and request:

extra tax deducted each pay

a fixed dollar amount per pay period

This spreads the tax over the year instead of a big bill in April.

Option 2 – Use RRSP Planning

Clients can reduce the problem by:

contributing to RRSPs

lowering taxable income

offsetting the extra tax from multiple jobs

Option 3 – Budget for Annual Payment

Some clients prefer to:

keep the cash during the year

pay once at filing time

👉 That’s okay—just make sure they understand the impact.

🧠 Key Lessons for New Tax Preparers

✔ Multiple T4s = likely CPP & EI refund ✔ Refund doesn’t mean no tax owing ✔ Always explain the “two-employer tax gap” ✔ Provide proactive payroll advice ✔ Don’t let clients be shocked in April

📋 Your Professional Checklist

When you see multiple T4 slips:

Confirm CPP/EI overpayments are calculated

Review total income bracket

Warn client about possible balance owing

Discuss TD1 adjustment

Explore RRSP options

🚀 Pro Tip

Clients judge you not by how fast you enter T4s—but by:

💬 how clearly you explain 💡 how well you prevent surprises 🤝 how proactive your advice is

Master this conversation and you’ll already be ahead of many tax preparers!

💰 RRSP Contributions – Overcontributions, Undeducted Amounts & Best Practices

📘 Why RRSPs Matter for Every Tax Preparer

RRSPs are one of the most powerful tools in Canadian tax planning—but also one of the most confusing for beginners.

As a tax preparer, you must understand:

how contributions are entered

what can be deducted this year

what must be carried forward

and what triggers penalties 🚨

Let’s break it down step-by-step in plain language.

🧾 Step 1 – Start With the Contribution Limit

Before entering ANY RRSP slip, always ask:

“Does the client actually have room?”

Where to Find the Limit

You can confirm the RRSP deduction limit from:

CRA Notice of Assessment

CRA My Account

Represent a Client portal

👉 Never rely on guesses—this number controls everything.

✏️ Entering RRSP Slips Correctly

Best Practice #1 – Enter Slips Individually

Don’t lump amounts together!

If a client has:

$8,000 contributed during the year

$1,600 in the first 60 days of next year

👉 Enter them as TWO separate slips.

Why?

✔ Easier review ✔ Matches CRA records ✔ Prevents double-claiming next year

Best Practice #2 – Track Receipt Numbers

Some clients (intentionally or not) try to:

reuse first-60-day slips next year

claim the same RRSP twice

Adding the receipt number in your file protects you.

🧠 Deduct Now or Later?

Just because a client contributed RRSPs does NOT mean they must deduct them this year.

Example:

Client contributed: $9,600 Wants to deduct: $8,000 only

👉 That is perfectly allowed.

The remaining $1,600 becomes:

✔ Undeducted RRSP contributions ✔ Carried forward automatically ✔ Available next year

🚨 Overcontribution vs Undeducted – BIG Difference

This is where new preparers get confused.

1. Undeducted Contribution (SAFE)

Happens when:

Client has enough RRSP room

Chooses not to deduct full amount

✅ No penalty ✅ Can keep funds in RRSP ✅ Deduct later

2. Overcontribution (DANGEROUS)

Happens when:

Client contributes MORE than their limit

Exceeds $2,000 lifetime cushion

❌ Subject to 1% PER MONTH penalty ❌ CRA form required ❌ Must usually withdraw funds

🧮 What Happens With an Overcontribution?

CRA Forms Involved

📄 T1-OVP – Overcontribution Tax

Calculates monthly 1% penalty

Depends on exact contribution dates

CRA often recalculates this

📄 T3012A – Tax Waiver on Withdrawal

Allows RRSP withdrawal

WITHOUT withholding tax

Prevents double taxation

👉 Critical step—otherwise the bank will withhold tax as if it were income!

🗓 First 60 Days Rule Explained

RRSPs contributed in:

📅 January & February

Can be:

reported on THIS year’s return

deducted THIS year or NEXT year

But they must still be reported now even if not deducted.

✅ Practical Workflow for Tax Preparers

Every RRSP file should include:

✔ Verified CRA limit ✔ All slips entered separately ✔ First-60-day amounts clearly shown ✔ Decision on deduction vs carryforward ✔ Check for overcontribution risk

🛑 Common Beginner Mistakes

❌ Entering one total instead of slips ❌ Forgetting first-60-day reporting ❌ Ignoring contribution limit ❌ Confusing overcontribution with undeducted ❌ Not warning client about penalties

💡 Client Advisory Tips

Tell clients:

Don’t overcontribute “just to save tax”

Wait for Notice of Assessment before large deposits

RRSPs don’t have to be deducted immediately

Penalties can grow fast

🧩 Key Takeaways

Contribution within limit → deduct now or carry forward

Over limit ≤ $2,000 → no penalty

Over limit > $2,000 → 1% monthly tax

First 60 days → must be reported in current return

🏠 Reporting the Home Buyers’ Plan (HBP) – Repayments, Missed Payments & Early Payoff

📌 What Is the Home Buyers’ Plan?

The Home Buyers’ Plan (HBP) allows Canadians to withdraw up to $35,000 (previously $25,000) from their RRSP to buy or build a qualifying home—without paying tax on the withdrawal.

But there’s a catch 👇 You must repay the amount to your RRSP over 15 years, starting usually in the second year after the withdrawal.

If you don’t repay? 👉 The required amount becomes taxable income for that year.

🧮 How HBP Repayments Work

Every year CRA calculates:

Your annual required repayment

Your remaining HBP balance

Whether you made enough RRSP contributions to cover it

Example: If someone withdrew $25,000, their yearly repayment is:

$25,000 ÷ 15 = $1,667 per year

This amount must be designated from RRSP contributions on the tax return.

✍️ Step-by-Step: Reporting HBP on a Tax Return

When preparing a return:

Enter all RRSP contributions as usual

Scroll to the HBP repayment section

Allocate part of the RRSP contributions to HBP

Important Concept

Total RRSP contributed ≠ RRSP deduction

👉 Part of the contribution may be used to repay HBP and cannot also be deducted.

🔍 Example Scenario

Client contributed to RRSP this year: $9,600 Required HBP repayment: $1,667

Result:

$1,667 → goes toward HBP

$7,933 → available as RRSP deduction

💡 This split is reported on Schedule 7 of the tax return.

🚨 What Happens If the Client Doesn’t Repay?

Two common situations:

1. Client contributed to RRSP but forgot to designate HBP

CRA will automatically:

Reassess the return

Allocate the required amount to HBP

Reduce the RRSP deduction

👉 The expected refund will be LOWER than originally calculated.

2. Client made NO RRSP contribution

This is more serious.

If required repayment = $1,667 and no RRSP deposit was made:

👉 $1,667 becomes taxable income on line 129 of the T1.

This can create an unexpected tax bill 💸.

⏩ Paying Off HBP Early – Is It Smart?

Clients are allowed to:

Repay more than the minimum

Even repay the FULL balance at once

But from a tax perspective:

❗ Paying early often gives no advantage

Why?

HBP repayment does not create a deduction

RRSP contributions used for HBP cannot reduce income

Better strategy is usually:

Pay minimum to HBP

Use remaining RRSPs for deductions

🧠 When Early Repayment Might Make Sense

Early payoff can help if the client:

Wants smaller future annual obligations

Plans lower income in future years

Prefers to clear debts psychologically

May stop contributing to RRSPs soon

But purely for tax savings? 👉 Usually not beneficial.

✅ Best Practices for Tax Preparers

Always verify:

✔ HBP balance from CRA account ✔ Required annual repayment ✔ RRSP slips for the year ✔ First-60-day contributions ✔ Whether client intends early repayment

❌ Common Mistakes to Avoid

Forgetting to ask about HBP status

Entering RRSP deduction without HBP allocation

Assuming CRA will “fix it later”

Not warning clients about taxable inclusion

Confusing HBP with Lifelong Learning Plan

🗣 Client Communication Tips

Tell clients clearly:

“Your RRSP deposit must be designated to HBP.”

“If you skip a year, CRA will add it to income.”

“Early payoff doesn’t usually save tax.”

A 2-minute conversation can prevent a nasty reassessment letter 📬.

📦 Key Takeaways

HBP requires 15 annual repayments

Repayment comes from RRSP contributions

Missed payment = taxable income

Early payoff allowed but rarely optimal

Schedule 7 is the core reporting form

💼 Employment Expenses, T2200 & Real-Life Examples Every Tax Preparer Must Know

Employment expenses are one of the most reviewed areas by CRA—and one of the easiest places for new tax preparers to make mistakes. Just because a client spent money for work does NOT mean it is deductible.

Everything revolves around one critical document → Form T2200.

Let’s break this down step-by-step like you’re sitting in front of your first real client 👇.

📄 What Is Form T2200 and Why It Matters

👉 T2200 = Declaration of Conditions of Employment

This form must be:

Completed by the EMPLOYER

Signed and dated

Kept on file by the taxpayer

Available if CRA asks for proof

❗ Without a valid T2200 → employment expenses are NOT allowed.

No signature = No deduction. Period.

🧾 Common Expenses Employees Try to Claim

Depending on the job and T2200 answers, employees may deduct:

🚗 Vehicle expenses

📱 Cell phone & internet (business portion only)

🖥 Home office costs

✈ Travel expenses

✉ Supplies

🍽 Meals (limited)

🧾 Accounting/legal (for commission employees)

But eligibility depends 100% on what the T2200 says.

🚗 Example 1 – Taxable Car Allowance

Situation

Client receives:

$600 per month car allowance

Included in T4 box 40 → $7,200 taxable

Must use own vehicle for work

Keeps a mileage log

Actual annual vehicle costs:

Gas, insurance, repairs

Lease payments

Total: $8,530

Business km: 11,480

Total km: 17,418

Result

Allowed deduction on T777:

✔ Business portion of vehicle = $8,530 ✔ Cell phone (2/3 business) = $856 ➡ Total employment expenses = $9,386

💡 Because the allowance was taxable, the employee can deduct actual costs.

🚫 Deducting without signed T2200 🚫 Claiming reimbursed expenses 🚫 Forgetting mileage log 🚫 Using 100% of cell phone 🚫 Mixing personal & business km 🚫 Not checking employment period dates

🧠 Best Practices for Tax Preparers

Always Ask Clients:

Do you have a signed T2200?

Were you reimbursed for ANY costs?

Do you keep a mileage log?

Is allowance on T4 box 40?

Commission or salary only?

Keep on File:

T2200 copy

Mileage log

Receipts

Lease agreements

Cell phone bills

💵 Applying for the GST/HST Rebate – Rules, CRA Reviews & Smart Client Advice

When employees claim employment expenses, there is one extra benefit many new preparers overlook — the GST/HST rebate. This rebate allows an employee to recover the sales tax paid on deductible employment expenses if certain conditions are met.

Let’s break this down in a beginner-friendly way so you know:

Who qualifies

How to calculate it

Where it appears on the return

The CRA risks involved

When it might NOT be worth claiming

🔎 What Is the GST/HST Rebate for Employees?

If an employee:

Is required to incur employment expenses, and

Has a valid T2200 from the employer, and

The employer is registered for GST/HST,

then the employee may claim back the GST or HST paid on those expenses.

👉 This is NOT automatic. 👉 It must be calculated and reported separately on the tax return.

✅ Which Expenses Qualify?

Only expenses that are already deductible on Form T777 can generate a rebate, such as:

🚗 Vehicle operating costs (gas, repairs, lease)

📱 Cell phone (business portion)

🖥 Home office expenses

✈ Travel costs

🧾 Supplies

❌ Expenses with no GST/HST do NOT qualify, for example:

Insurance

License & registration

Interest on car loans

🧮 How the Rebate Is Calculated

In an HST province (like Ontario), the rebate is based on:

HST portion = 13 ÷ 113 × eligible expense

Example:

Business vehicle costs: $8,530

Cell phone (business portion): $856

HST rebate ≈ $883

This amount becomes a refundable credit on the personal return.

📍 Where Does It Appear on the T1?

Reported on Line 45700 – GST/HST Rebate

Increases the client’s refund or reduces balance owing

BUT… there’s a catch ⬇

⚠️ The “Next Year Income” Trap

The rebate is not free money forever.

📌 The amount received must be included in income next year (Line 10400).

So:

Client gets $883 refund this year

Next year they might pay $300–$400 tax on it

This reduces the real benefit.

🚨 CRA Review Risk – Very Important

GST/HST rebates are a major CRA audit trigger.

Claiming the rebate often leads CRA to review:

The T2200

Mileage logs

Receipts

Entire T777 employment expenses

💥 A small rebate can open the door to a big reassessment.

🧠 Professional Judgment – When NOT to Claim

You should think twice if:

Rebate is only $200–$400

Client records are weak

Mileage log is incomplete

Some expenses are estimates

T2200 wording is vague

👉 Risking a $9,000 expense claim for a $300 rebate is often NOT smart.

🗣 How to Explain This to Clients

Tell them:

“Yes, you can get the GST back — but CRA often reviews these claims. If your records are perfect, we’ll claim it. If not, the rebate may not be worth the risk.”

This builds trust and protects you as the preparer.

🧩 Eligibility Checklist

Before claiming, confirm:

✔ Employer is GST/HST registrant

✔ Signed T2200 on file

✔ Expenses already allowed on T777

✔ Receipts kept

✔ Mileage log available

✔ No reimbursement from employer

If any box is NO → do NOT claim the rebate.

🛠 Best Practices for Tax Preparers

Keep copy of T2200 in file

Separate GST/HST amounts on worksheets

Never claim tax on insurance or license fees

Warn clients about next-year income inclusion

Document the decision to claim or not claim

📌 Final Takeaways

GST/HST rebate = nice bonus, but not risk-free

Must flow from valid employment expenses

Triggers CRA scrutiny

Included in income next year

Use professional judgment every time

⚠️ Other Employment Income Issues Every Tax Preparer Must Watch For

Employment income is more than just copying numbers from a T4. Real-life client files come with gray areas, missing slips, and tricky reporting rules that can easily trigger CRA reviews. Below are the most common problem areas you’ll face as a new tax preparer—and how to handle them like a pro 💼.

🍽️ Tips & Gratuities – Service Industry Income

Clients who work as:

waiters/waitresses

bartenders

delivery drivers

hotel staff

hair stylists

often earn cash and electronic tips on top of their wages.

Key Rule 👉 ALL tips are taxable income

Even if:

the employer doesn’t include them on the T4

they were paid in cash

the client thinks “everyone ignores them”

Tips are still employment income subject to tax and CPP.

Modern Reality

Most tips today are paid by:

credit card

debit machine

online apps

This means employers often have full electronic records and may include tips directly on the T4. But not all employers do!

💬 How to Handle Client Questions

Clients often ask:

“How much should I report? 10%? 15% of sales?”

🚫 WRONG approach!

✔ Correct answer:

“You must report the actual tips you received. I can’t choose a percentage for you.”

As a preparer, your role is to:

ASK the question

DOCUMENT the client’s answer

REPORT what they tell you

Never guess or create a number for them.

🛑 Employment Insurance (EI) Clawback

EI benefits are reported on a T4E slip and included in income. But there’s a hidden trap:

🔁 EI Repayment Rule

If total income exceeds roughly $65,000, part of EI may have to be repaid.

The tax software will calculate:

📌 Line 23500 – EI income deduction

📌 Line 42200 – Social benefits repayment

👉 Clients are often shocked when EI becomes repayable after they return to a high-paying job.

Your job is to:

warn them in advance

explain it’s normal

show the calculation clearly

🧩 Line 10400 – “Other Employment Income” Risks

Anything placed on Line 10400 can trigger CRA attention.

Common examples:

cash wages not on a T4

tips not included by employer

informal payments from an owner-managed corporation

bonuses paid outside payroll

🚨 CPP Problem

Income on Line 10400 usually does NOT automatically calculate CPP.

CRA runs a “Line 104 Project” to find cases where CPP should have been paid.

✔ Proper Fix – CPT20 Election

If the income should be pensionable, file:

📄 Form CPT20 – Election to Pay CPP on Pensionable Earnings

This ensures:

CPP is correctly calculated

CRA won’t reassess later

client avoids penalties & interest

💼 Severance & Termination Pay

Severance often confuses clients because:

net pay ≠ letter amount

payments may be split over 2 years

different T4 boxes are used

Reporting Basics

Severance normally appears in Box 66 / Box 67

Flows to Line 13000 – Other Income

Still fully taxable

Tax Planning Opportunity 🎯

Employers sometimes:

pay part in December

pay part in January

This can:

split income across two years

reduce marginal tax

help avoid EI clawback

👉 Always review severance letters and timing!

🧠 Practical Checklist for Preparers

Whenever you see employment income, ask:

✔ Is the client in the service industry?

✔ Are tips fully reported?

✔ Is there a T4E with possible clawback?

✔ Any Line 104 income that needs CPP via CPT20?

✔ Severance paid across two years?

✔ Missing slips or informal payments?

📦 Pro Tips to Stay CRA-Safe

Document client answers about tips

Never invent percentages

Watch for EI repayment above $65k

Use CPT20 when required

Don’t rely on severance letters—use T4 reporting

Add detailed file notes 📝

🎯 Final Thought

Employment income seems simple—but it’s one of the most reviewed areas by CRA. A careful interview + proper forms = happy client & stress-free practice.

🧩 Allowable Business Investment Losses (ABIL) — Why They’re Hard to Claim (Beginner-Friendly Guide)

Allowable Business Investment Losses—often called ABILs—are one of the most misunderstood and heavily challenged areas in Canadian personal tax. If you’re a new tax preparer, this topic may seem intimidating… and honestly, you’re not wrong! ABILs are complex, frequently audited, and often denied if not documented perfectly.

But this guide breaks everything down in simple terms, with practical examples and checklists. By the end, you’ll understand:

What an ABIL is

Why ABILs are so hard to claim

What CRA looks for

Why ABILs trigger audits

Common real-world scenarios you will see as a tax preparer

How to prepare clients properly so their claim doesn’t get denied

📌 What Is an ABIL (Allowable Business Investment Loss)?

An ABIL is a special type of capital loss that comes from:

👉 Investing in a small business corporation, either by

Buying shares, or

Lending money to the corporation

If that business fails, you may be able to claim an ABIL.

📘 Why “ABIL” Is Special

Most capital losses can only offset capital gains.

BUT an ABIL is different:

🟢 You can deduct it against all other kinds of income, including:

Employment income

Business income

Interest income

Rental income

🔵 Only 50% of the business investment loss is deductible — this is the “allowable” part.

🚨 Why Are ABILs So Challenging to Claim?

ABILs are one of the most heavily reviewed and litigated tax items in Canada. CRA audits almost every ABIL claim over $10,000.

Here’s why.

⚠️ 1. CRA Believes Most ABIL Claims Are Invalid

ABIL rules are strict. CRA wants proof that:

The corporation was a Small Business Corporation (SBC)

The investment was genuine, not a disguised gift or related-party favour

The business is actually insolvent, bankrupt, or has ceased operations

The loss is real and final, not temporary

The taxpayer expected to earn income from the investment (wasn’t just helping family)

CRA denies about 90% of doubtful claims because taxpayers lack proper evidence.

⚠️ 2. ABIL Requires Both Corporate & Personal Tax Knowledge

Although the loss is claimed on a personal tax return, determining whether it qualifies is actually a corporate law and corporate tax analysis.

New tax preparers often miss these requirements:

✔ Was the company really a Small Business Corporation? ✔ Were proper share certificates issued? ✔ Was the loan properly structured? ✔ Does documentation prove the investment was valid and enforceable?

⚠️ 3. High Risk of Abuse

Many people attempt ABIL claims in these situations:

Investor “lends” money to a child’s corporation

No promissory note exists

No expectation of repayment

Company was not a qualifying SBC

Records are incomplete

The “loan” was actually a gift

CRA sees these constantly — most get denied.

⚠️ 4. ABIL Is Final — It Can’t Be Undone Later

Once an ABIL is claimed, CRA wants solid proof because:

It becomes part of a taxpayer’s non-capital loss pool

It can reduce income for future tax years

It may affect estate planning and business planning

Because it has long-term tax impact, CRA examines it closely.

📂 What CRA Usually Asks For (Be Prepared!)

If your client claims an ABIL, expect CRA to request the following:

📄 For Shares

Share certificates

Subscription agreements

Corporate minute book records

Evidence business was a Small Business Corporation

Proof the shares became worthless

🧾 For Loans

Signed loan agreements/promissory notes

Repayment terms

Interest terms

Proof loaned funds were actually used in the business

Proof the corporation is bankrupt/insolvent

🏚️ To prove business failure

Bankruptcy documents

Asset sale records

Closure notices

CRA correspondence showing the business has ceased operations

Without these documents, the ABIL will almost always be denied.

📘 Why ABILs Trigger Audits Almost Automatically

CRA has publicly stated that ABILs are an “audit flag.” Claims over $10,000–$15,000 are almost guaranteed to be reviewed.

This is because:

ABILs reduce tax significantly

Many are incorrectly claimed

Many involve related-party transactions (parents → children, friends → business)

Expect 90% likelihood of CRA review for any meaningful ABIL.

💡 Real-World Scenarios You Will See as a Tax Preparer

These situations are very common—and often denied:

👪 1. Parents lending money to their child’s corporation

Example: Mom and Dad “lend” $100,000 to help their child start a restaurant.

👉 Problem:

No loan document

No repayment terms

Loan was not made for the purpose of earning income

CRA considers it a gift

❌ Most of these ABIL claims get denied.

🏢 2. Shareholder invests money in their own small corporation that later fails

This is a legitimate scenario if documented properly.

CRA still requires proof:

✔ SBC status ✔ Share certificates ✔ Evidence of insolvency ✔ Proof investment became worthless

💼 3. Business owners invest in another owner’s corporation

Example: Two entrepreneurs invest in each other’s companies.

These may qualify IF:

Money was invested for income purposes

Proper agreements were signed

Corporation meets SBC rules

⚰️ 4. The corporation simply “stopped operating” — but no bankruptcy

This is the trickiest.

CRA does not allow ABIL just because the business closed.

You must prove:

No assets left

No ongoing business activity

No reasonable chance of repayment

No share value remaining

🧠 Pro Tax Tip Box

💡 ABIL is not a simple deduction — it’s a legal argument. Every ABIL claim needs evidence, documentation, and ideally a tax practitioner who understands corporate structure.

📝 How an ABIL Is Reported on the Tax Return

If the investment meets all conditions:

The full loss goes on Schedule 3

Only 50% is allowed

It becomes an ABIL

It flows to line 21700

If unused, it becomes a non-capital loss carried forward/back

Reporting is easy — qualifying the loss is the hard part.

📚 Summary: What You MUST Remember as a New Tax Preparer

✔ ABILs are one of the most audited and denied claims in Canada ✔ Requires both personal and corporate tax knowledge ✔ CRA disallows most claims due to poor documentation ✔ Never file an ABIL without checking SBC status & documentation ✔ Expect CRA to contact you within months of filing ✔ Reporting is simple — proving eligibility is complex ✔ ABIL claims must be backed by strong, complete paperwork

⭐ Final Tip

Most ABIL claims fail because taxpayers treat business investments casually. Your job as a tax preparer is to ensure formality, evidence, and documentation at every step.

🌟 General Review of ABIL Rules — What Every Personal Tax Preparer Must Know

Allowable Business Investment Losses (ABILs) are one of the most powerful—yet most complicated—deductions in Canadian personal tax. As a tax preparer, understanding the core rules, qualifying criteria, and tax implications is essential. This guide breaks the topic down into simple, beginner-friendly language (with plenty of visuals) so you can confidently handle ABIL situations for clients.

🧠 What Exactly Is an ABIL?

An Allowable Business Investment Loss is a special type of capital loss that arises when a taxpayer invests in a Canadian small business corporation, and that investment becomes worthless.

🟦 It can come from:

❗ Selling shares of a small business corporation at a loss

❗ Lending money to a corporation and not getting it back

🟩 Why ABIL is special: Unlike normal capital losses (usable only against capital gains), an ABIL is 50% deductible against any type of income, including:

Employment income

Business income

Rental income

Interest income

This makes ABILs extremely valuable—if they qualify.

💰 How ABILs Are Calculated

ABILs follow the same structure as capital gains/losses:

Type

Inclusion Rate

Deductible Against

Capital Loss

50%

Only Capital Gains

Business Investment Loss

—

—

ABIL (50% of BIL)

50%

All income types

🔍 Formula: If you lose $40,000 on an investment in a qualifying corporation: ➡️ Only 50% = $20,000 ABIL ➡️ Deductible against all types of income

📆 Carryforward Rules for ABIL

ABILs have special time rules:

⏳ First 10 years

✔ Can be deducted against all sources of income ✔ If unused → remains an ABIL

⏩ After 10 years

🔁 The unused ABIL becomes a capital loss ✔ Capital losses carry forward indefinitely ✔ Usable only against capital gains

⚰️ In the year of death

Capital losses turn back into non-capital losses, usable against all income.

🔍 Important — ABIL Can Be Reduced by Capital Gains Exemption

If a taxpayer previously used the Lifetime Capital Gains Exemption (LCGE), it may reduce the ABIL they can claim.

📝 Why? Both benefits relate to small business corporation shares, and the law prevents taxpayers from stacking these incentives unfairly.

🧱 Where Do ABILs Come From?

Two main sources:

🆔 1. Shares of a Canadian-Controlled Private Corporation (CCPC)

This includes shares the taxpayer:

Originally purchased

Received when investing in the startup

Sold at a loss

Cannot sell because the corporation failed

💵 2. Debt Owing to the Taxpayer by a CCPC

If someone lends money to a corporation and can’t recover it, the unpaid loan may qualify as a Business Investment Loss.

🧩 Four Mandatory Qualifiers for ABIL

To claim an ABIL, the following four conditions MUST be met. CRA does not compromise on these.

🟦 1. The loss must come from shares or debt of a CCPC

A Canadian-Controlled Private Corporation is:

Privately owned

Controlled by Canadian residents

Not publicly listed

📘 Tax preparer tip: Always confirm CCPC status—look at shareholder registers, minutes, and tax filings.

🟦 2. The corporation must be a Small Business Corporation (SBC)

This means the business must earn active business income.

✔ Examples of active businesses:

Restaurants

Retail stores

Manufacturing

Trades

Professional practices

❌ Does not include corporations earning:

Rental income

Passive investment income

Portfolio income

Personal service business income

📉 Important: Share losses from real estate corporations do NOT qualify for ABIL.

🟦 3. If the investment was a loan, interest must have been charged

CRA requires proof that:

There was a real expectation of income, and

The loan was a real investment, not a gift

📌 Notes:

Interest does not need to be paid (company may be insolvent)

But the loan agreement must show interest was owed

🟥 Exception: If the lender is a shareholder, interest is not mandatory because shareholders can earn income through dividends instead.

🟦 4. The shares or debt must be disposed of — or deemed disposed of

You cannot claim an ABIL unless the investment is:

Sold

Written off

Proven worthless

OR deemed disposed of using special tax elections

📝 The most common tool: 🔹 Section 50(1) Election This allows taxpayers to claim a loss even when the corporation is insolvent and shares cannot be sold.

🔒 CRA’s Two-Part Test: Qualify + Prove It

CRA requires:

1️⃣ The ABIL must meet all four qualifiers

AND

2️⃣ You must prove it with documentation

Clients often meet the rules but fail to document them properly, leading CRA to deny the ABIL.

📦 What Documentation Does CRA Expect?

📄 For Share Investments

Share purchase agreements

Share certificates

Corporate minute book

Proof of CCPC status

Evidence shares became worthless

🧾 For Loans

Signed loan agreement

Interest terms

Promissory notes

Evidence business used the loan

Evidence of insolvency

🏚️ For Business Failure

Bankruptcy documents

Final tax returns

Letters showing the business ceased operations

Proof of asset liquidation

Without documentation, CRA will almost always deny the claim.

🔥 Special Notes for New Tax Preparers

🟣 ABILs are high-risk audit items

Expect CRA review for any ABIL over $10,000–$15,000.

🟠 ABILs are heavily litigated

Over 240+ tax court cases exist on this topic.

🟡 ABIL reporting is simple — qualifying is complex

Most of your work involves gathering and verifying proof.

📘 Quick Reference Box — The Four ABIL Qualifiers

💼 Must be CCPC shares or loans 🏭 Must be active business (not rental/investment) 💲 Loan must charge interest (except shareholders) 📉 Investment must be disposed of or deemed disposed of

👍 Final Thoughts for New Tax Preparers

ABILs are one of the most valuable deductions in the tax system but also one of the most difficult to claim correctly. Your job is not just completing the tax form—it’s ensuring the investment truly qualifies and is properly documented.

A skilled tax preparer can save clients thousands, but only with a strong understanding of these rules.

💼 Common Scenarios Where an ABIL Can Be Claimed — Beginner’s Guide for Tax Preparers

Allowable Business Investment Losses (ABILs) are one of the most valuable personal tax deductions, but also one of the most complex. As a tax preparer, it’s important to know where ABILs typically arise, so you can spot opportunities for your clients—and avoid costly mistakes. This guide explains the most common real-world scenarios where ABILs may be claimed, with practical tips, examples, and documentation considerations.

🟢 1. Investments in Corporations That Become Insolvent

One of the most frequent ABIL scenarios involves:

Buying shares in a corporation

Lending money to a corporation

When the corporation fails or becomes insolvent, the investor may claim an ABIL for the lost investment.

Example:

A client invests $50,000 as an angel investor in a small startup.

The startup closes after two years, and the shares are now worthless.

The client may be eligible to claim 50% of the loss against all types of income, provided the investment qualifies as a CCPC share or shareholder loan.

💡 Pro Tip: Always confirm CCPC status and that the business was actively operating (not a passive investment) before claiming ABIL.

🟢 2. Investments in Family or Friends’ Small Businesses

Many small businesses are funded by family or friends through:

Share purchases

Loans to the business

If the business fails and repayment is impossible, these losses can qualify as an ABIL.

Example:

Parents invest $20,000 in their child’s small business.

The business closes and cannot repay the investment.

Parents may claim an ABIL—but only if:

The business qualifies as a CCPC

The investment meets all ABIL qualifiers

Proper documentation exists

💡 Note: Investments in family businesses are heavily scrutinized by CRA. Documentation and proof of intent to earn income are essential.

🟢 3. Owner-Manager Investments in Their Own Corporation

Perhaps the most common ABIL scenario for small practitioners involves owner-managers:

They invest personal funds to start or maintain a corporation

They may purchase shares or lend personal money to the business

The business ultimately fails and funds cannot be recovered

Key Points:

The investment must be in a CCPC with active business income

Loans must document interest owed (even if unpaid)

Shares or loans must be disposed of or deemed disposed of via a Section 50(1) election

📝 Tax preparer tip: Owner-managers often overlook ABIL claims, but with proper guidance and documentation, this is an opportunity to save significant taxes.

🟢 4. Victims of Scams or Fraudulent Businesses

If a client invests in a corporation that turns out to be fraudulent, it may be possible to claim an ABIL—if proof exists:

Police or legal reports verifying the fraud

Bank statements showing the investment

Correspondence with the company confirming the loss

⚠️ Caution: Documentation is crucial. Without it, CRA will likely deny the ABIL. Fraud cases are technically allowed, but proving them is challenging.

🟢 5. Investment Clubs or Corporations That Invest in Small Businesses

Some clients invest indirectly through investment corporations or clubs:

The corporation collects funds from multiple investors

It invests in various small businesses (e.g., tech startups, restaurants, cafes)

If one of those businesses fails, investors may be eligible for ABIL

❌ Note: ABILs do not apply to investments in:

Publicly traded securities

Real estate companies

Passive portfolio investments

💡 Tip: Always trace the investment to a qualifying small business to determine ABIL eligibility.

🟢 6. Payments Made to Cover CRA Liabilities of a Corporation

In some cases, shareholders may pay corporation liabilities such as:

GST/HST

Payroll taxes

Other CRA obligations

If these payments are made because the corporation cannot pay, they may be considered an ABIL, because funds were directly used to support the business.

Example:

A director pays $15,000 in unpaid payroll taxes for a corporation.

The corporation becomes insolvent and cannot repay.

The director may claim an ABIL for the amount paid, with proper documentation.

⚠️ Important: These situations are complex and may require a tax lawyer or senior review.

📦 Documentation Checklist for Common ABIL Scenarios

For any ABIL claim, ensure the following is available:

✅ Proof of investment (share certificates, loan agreements) ✅ Corporate status (CCPC confirmation, minute books) ✅ Evidence of active business operations ✅ Proof of insolvency or failed business ✅ Interest terms for loans (if applicable) ✅ Section 50(1) elections for deemed dispositions ✅ Any additional correspondence, legal, or CRA documentation

💡 Pro Tip: Keep a separate folder for each client’s ABIL documentation—it’s your best defense during a CRA audit.

💡 Key Takeaways for Tax Preparers

ABILs arise in specific, common scenarios:

Corporate insolvency

Family or friends’ businesses

Owner-manager losses

Fraudulent investments

Investment clubs investing in small businesses

Payment of corporate liabilities

Documentation is everything—without proof, CRA will deny the claim.

ABILs can provide significant tax savings, but require careful verification.

Always confirm CCPC status, active business, and qualifying loss before claiming.

⭐ Pro Tip Box: “ABILs are often overlooked by taxpayers, but as a tax preparer, you can become a hero for your clients by spotting these opportunities—provided you gather and verify the proper documentation!”

📝 Claiming ABIL on the T1 Return & Electing Under Section 50-1 of the ITA

Claiming an Allowable Business Investment Loss (ABIL) on a personal tax return may seem straightforward, but there are critical nuances that every tax preparer must understand—especially when dealing with owner-managed businesses or investments that cannot be sold. This section breaks it down step-by-step with examples, practical tips, and guidance on the Section 50-1 (subsection 51) election, so you can confidently prepare ABIL claims for clients.

💼 1. How ABIL Is Claimed on the T1 Return

An ABIL is claimed much like a capital loss, but with the key difference that it can offset all sources of income, not just capital gains.

Step-by-Step Process:

Calculate the Loss

Determine the original investment amount (shares purchased or loaned)

Deduct any amount recovered (sale proceeds, partial repayment)

Include related expenses, e.g., legal fees or consulting fees directly linked to the investment

Example:

Share purchase: $125,000

Amount recovered: $10,000

Legal & consulting fees: $2,985

Total ABIL: $117,985

50% deductible: $58,993

Enter on the T1 Return

Line 21700: Enter the allowable portion of the ABIL (50% of total loss)

Box 21699: Enter the gross loss (full amount before 50% deduction)

Software Assistance Most tax preparation software includes an ABIL worksheet, which calculates the loss and generates the appropriate entries for the T1 return automatically.