Preparing for the TICO Supervisor/Manager exam means understanding how investigations work and what happens if someone breaks the rules. This chapter will help you learn about proper conduct, investigations, offences, and penalties in a simple, easy-to-follow way.

Conduct: Acting Honestly and Legally

The Travel Industry Act, 2002 and Ontario Regulation 26/05 exist to protect consumers buying travel services from registered travel sellers in Ontario.

As a registrant, you must act with honesty and integrity in everything you do. Proper conduct isn’t just about following some rules—it’s about complying with all the requirements in the legislation. If you follow the law, you’re acting correctly.

The Statutory Director

Known as the Director, appointed by TICO’s Board.

Has special legal powers under the Act.

Not the same as a Registrar or a Board member.

Section 30 of the Act: If the Director sees someone isn’t following the Act or Regulation, they can apply to the Superior Court of Justice for an order to make the person comply. Individuals can appeal these orders to the Divisional Court.

TICO also has inspectors who can check registrants to ensure compliance. If there’s a suspected violation, cases may go to investigators who can officially inquire and possibly lead to charges.

Investigations: How TICO Looks into Violations

Investigators’ Role (Section 19)

The Director can appoint investigators.

Investigators receive a certificate of appointment, which they must show on request.

They are authorized to officially examine potential violations.

Search Warrants (Section 20)

Before entering a non-registrant’s premises, investigators need a search warrant from a Justice of the Peace.

A warrant may allow investigators to:

Enter the premises and examine/seize items listed in the warrant.

Access business computers or data storage.

Use investigative procedures listed in the warrant.

Conditions for Search Warrants

Investigators must believe a person broke the Act or Regulation.

They must also believe evidence is in a building or place.

Special permission is needed to enter private homes.

Key points:

Experts can assist investigators.

Warrants usually allow entry 6 a.m. to 9 p.m. unless otherwise stated.

Warrants expire after 30 days, unless extended.

Police may assist and use reasonable force.

No one can obstruct an investigation or destroy relevant items.

Items in plain view that relate to the violation can be seized.

Seized items must be returned promptly.

Exigent Circumstances (Section 21)

Sometimes investigators may search without a warrant if it’s an emergency.

Police assistance may be used, and reasonable force is allowed.

This does not apply to homes.

Improper Conduct: What Not to Do

The law also lists actions that are considered improper:

Falsifying information or documents related to travel services.

Providing false or deceptive information, or encouraging others to do so.

Making misleading statements in advertisements or publications.

Avoiding these actions is key to staying compliant and protecting consumers.

Penalties for Offences: What Happens if You Break the Law

Section 31 – Offences

A registrant can be guilty of an offence for:

Providing false information on applications or returns.

Failing to comply with orders or directions under the Act.

Breaking any section of the legislation.

Penalties differ for individuals vs. corporations:

Individuals: Up to $50,000 fine, up to 2 years less a day in jail, or both.

Corporations: Up to $250,000 fine.

Corporate officers may also be liable if they didn’t take reasonable care to prevent the offence.

Time Limit:

No prosecution can start more than 2 years after TICO’s Director knew about the violation.

Note: Violating TICO’s Code of Ethics alone is not considered an offence under the Act.

Section 32 – Orders for Compensation or Restitution

Courts may order convicted persons to pay compensation to victims or insurers/Travel Industry Compensation Fund.

Restitution means repairing the loss suffered by another party.

Sections 33 & 34 – Defaulting on Fines

If a fine isn’t paid for 60+ days, the Director can:

Report the default to a consumer reporting agency.

Place a lien on the person’s property.

Once the fine is paid, the lien or report must be removed.

A lien is a legal claim on property until a debt is paid.

Wrapping Up Chapter 10

You’ve now completed Chapter 10 – Investigations and Offences. Understanding investigations, improper conduct, and penalties will help you stay compliant and protect consumers.

Next Steps:

Take the voluntary online quiz on ‘MyTICO’ for this chapter.

Try the voluntary sample exam to test your readiness.

After preparing with quizzes and sample exams, take the final exam to complete your Supervisor/Manager certification.

Good luck! Staying honest, knowing the rules, and understanding penalties will make you a confident and competent TICO Supervisor/Manager.

(TICO Supervisor/Manager Level Study Guide — Chapter 9.1)

When consumers are unhappy with a travel service, TICO (Travel Industry Council of Ontario) ensures there is a fair, transparent process to handle their complaint. This process protects consumers and also gives registrants (travel agencies or wholesalers) a fair chance to resolve issues directly before TICO steps in.

🧭 Overview

TICO’s complaint handling system encourages resolution at the business level first. Only if the issue cannot be resolved between the consumer and the registrant does TICO get directly involved.

Here’s a visual guide to the process:

Step-by-Step Process

Step 1: Consumer Has a Complaint

The consumer experiences a problem or is unhappy with a travel service purchased through a TICO registrant.

Step 2: Complaint to the Registrant

The consumer must first contact the travel agency or tour operator directly to try to resolve the issue.

If the registrant resolves the complaint to the consumer’s satisfaction, the matter is closed.

Step 3: Consumer Approaches TICO

If the consumer is not satisfied with how the registrant handled the complaint, they can contact TICO for help.

TICO will first refer the consumer back to the registrant, giving the business another chance to resolve the issue before TICO intervenes formally.

Step 4: Filing a Complaint with TICO

If the consumer remains dissatisfied, they can file a formal complaint with TICO against the registrant. TICO then starts an official review process.

Step 5: TICO Requests Response from the Registrant

TICO contacts the registrant and requests a written response to the complaint. This letter will reference any applicable laws or regulations under the Travel Industry Act, 2002 or Ontario Regulation 26/05.

The registrant must then provide a detailed, written explanation of their position to TICO.

Step 6: TICO Assesses the Complaint

TICO’s Complaints Staff review all the evidence and correspondence to determine:

Whether the registrant addressed the issue properly

Whether there are any apparent breaches of the Travel Industry Act or its Regulations

Whether the case should be referred to the Compliance Department for further investigation

Step 7: TICO Communicates the Outcome

Once the review is complete, TICO writes to the consumer to explain:

TICO’s findings and position

Any refund or compensation (if applicable)

Whether the file will be referred to the Compliance Department for separate review

After this, the complaint process is complete.

⚖️ Important Notes

TICO’s goal is to ensure that complaints are resolved fairly and consistently.

TICO does not force a registrant to pay compensation unless there’s a proven breach.

TICO may take disciplinary or compliance action if it finds evidence of regulatory violations.

The consumer may still seek civil remedies (e.g., Small Claims Court) if unsatisfied with TICO’s resolution.

📘 Study Tip for the TICO Exam

TICO exam questions about this topic often test your understanding of the order of steps in the complaint process. Memorize the sequence:

TICO’s complaint process gives travel businesses every opportunity to resolve customer problems internally before formal investigation. This ensures fairness for both sides and keeps Ontario’s travel industry accountable and transparent.

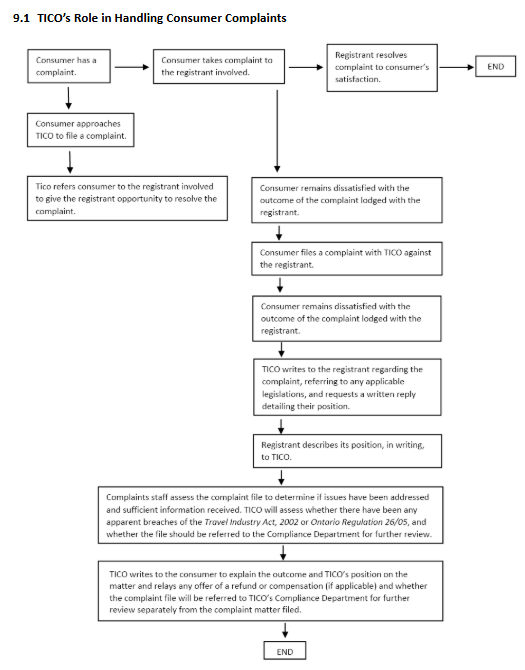

9.1 The Complaint Handling Procedure

TICO has a formal process for handling consumer complaints. Figure 9.1 (below) shows the complaint flow from start to finish. Let’s break it down into clear steps so you can easily remember it for your exam.

Step 1: The Consumer Contacts the Registrant

Before TICO gets involved, the consumer must first contact the travel retailer or wholesaler directly to try to fix the problem.

Consumers are asked to:

Put the complaint in writing.

Explain why they are unhappy.

Suggest how the issue could be resolved.

The complaint must be against an Ontario-registered travel retailer or wholesaler, or someone acting as an unregistered travel retailer in Ontario.

If the registrant resolves the complaint to the consumer’s satisfaction, the process ends here.

Step 2: The Consumer Files a Formal Complaint with TICO

If the problem is not solved, the consumer can then submit a complaint to TICO.

Here’s what happens:

TICO sends the consumer a complaint form.

The consumer fills it out and returns it with supporting documents such as:

Receipts

Tickets

Emails or messages between the consumer and registrant

Photos or other proof

By signing the form, the consumer gives TICO permission to share their information with:

The registrant involved

Other government or non-government sources (if necessary)

Step 3: TICO Requests the Registrant’s Response

Once TICO receives the complaint, it sends a copy to the registrant and asks for a written response. TICO also points out any parts of the Act or Regulation that apply to the issue.

If TICO suspects a possible breach of the law, it may ask the registrant to address specific concerns.

Section 16 of the Act

All registrants who receive a written request for complaint information from the Registrar must respond in writing as soon as possible.

Step 4: TICO Reviews the Complaint

TICO staff carefully review the entire complaint to decide:

Did the registrant respond properly and completely?

Are there any apparent breaches of the Act or Regulation?

Is more information needed (from the registrant or a third party)?

Should the case be referred to Compliance or the Registrar?

Has the registrant offered any compensation or goodwill gesture?

If TICO finds a potential compliance issue, it refers the file to the Compliance Department or Registrar for further review.

⚠️ Important: Even if the Compliance Department gets involved, TICO’s complaint process is separate from compliance actions. TICO does not update the complainant about compliance outcomes.

Step 5: TICO Communicates the Outcome

After TICO finishes its review, the consumer receives a letter outlining:

Confirmation that the registrant responded

A summary of the registrant’s position

Details of any compensation or goodwill offer

Whether the complaint revealed any breaches of the Act or Regulation

References to the specific legal sections that apply

Notice if the file was referred to the Compliance Department

An explanation that compliance reviews aim to fix breaches, not to get extra compensation for the complainant

A reminder that TICO cannot force a registrant to pay compensation or impose a settlement

If the consumer is still unhappy, TICO explains they may choose to:

Pursue legal action (e.g., Small Claims Court)

Consult a lawyer for further advice

TICO also notifies the registrant that the complaint file has been closed.

When Resolution Isn’t Possible

If a complaint cannot be resolved, TICO provides information on other options the consumer can explore, such as pursuing the issue through legal or other dispute resolution channels.

9.2 TICO’s Role in Handling Registrant-to-Registrant Complaints

Usually, TICO does not handle disputes between registrants (such as one agency vs. another). However, there are exceptions — specifically when there are financial or compliance concerns under the Act.

In these cases, TICO’s goal is to protect consumers and the integrity of the industry, not to act as a debt collector.

Example Scenario

Let’s say Registrant A stops working with Registrant B because B issued several bad cheques for travel services.

Registrant A must:

Notify the Registrar in writing

Explain the reason for ending business with Registrant B

TICO may investigate and perform a financial inspection on Registrant B to ensure:

Consumer funds are not at risk

Proper trust accounting is maintained

There is enough working capital

Section 21 of the Regulation

If a registrant stops dealing with another registrant because of apparent financial irresponsibility, they must notify the Registrar in writing and explain the reason.

9.3 Complaints Against TICO

TICO also has a process for handling complaints about TICO itself. These complaints are reviewed by the Governance and Nominations Committee, which is part of the TICO Board.

Committee’s Mandate

The committee ensures that TICO operates with:

Fairness

Transparency

Accountability

Its responsibilities include:

Reviewing and resolving complaints about TICO’s own conduct or service

Recommending improvements to complaint procedures

Setting standards for how complaints are handled

Tracking complaint trends to identify issues

Conduct and Conflicts of Interest

Committee members must act honestly and impartially. If a member has (or may have) a conflict of interest, they must disclose it and withdraw from any related discussions.

Types of Complaints the Committee Handles

The Governance and Nominations Committee looks at complaints such as:

Alleged abuse of process (e.g., unfair targeting or favoritism)

Consumer concerns about TICO not taking proper action against a registrant

Poor service or communication from TICO staff

Alleged breach of TICO’s access-to-information policy

Complaints the Committee Does Not Handle

The committee will not deal with:

Disputes about Compensation Fund decisions

Disputes about Notices of Proposal to Revoke Registration

Claims that the Act or Regulations are unfair or ineffective (unless tied to a specific complaint)

Standard of Review

Each complaint is reviewed based on a set of standards. The committee looks to:

Resolve the issue if possible

Identify broader problems that might need attention

While the committee cannot interfere with the Registrar’s legal duties, it can review how those duties are carried out to ensure fairness and accountability.

🧠 Study Tips for the Exam

Memorize the five main complaint steps (consumer → registrant → TICO → review → outcome).

Remember that TICO cannot force compensation — it ensures compliance, not settlements.

Understand when TICO will or won’t handle registrant-to-registrant complaints.

Know the role of the Governance and Nominations Committee in complaints against TICO.

✅ Summary

TICO’s complaints process is all about protecting consumers and maintaining industry integrity. It encourages direct resolution first, ensures fair review of all complaints, and keeps both consumers and registrants accountable under Ontario law.

Understanding what TICO expects from travel agencies and wholesalers

Managing money and keeping proper records are some of the most important parts of running a travel business in Ontario. TICO wants to make sure every registered travel agency and wholesaler handles their finances honestly and transparently — and that they’re financially stable enough to protect consumers.

This chapter will help you understand:

What financial reports must be submitted

How often they must be filed

Who can prepare them

What happens if the rules aren’t followed

These rules are found under Section 22 of the Regulation.

💼 8.1 Financial Statement and Document Reporting Requirements

Every TICO registrant (that means every travel agency or wholesaler registered with TICO) must file financial statements or a verification statement with TICO at least once a year. The type of document you file depends on how much travel you sell in Ontario each year.

Let’s break this down.

📊 Annual Sales Determine Reporting Type

Annual Ontario Sales

What You Must File

Deadline

Less than $2 million

Verification statement or annual financial statement

Within 3 months (90 days) of year-end

$2 million – less than $10 million

Annual financial statement

Within 3 months (90 days) of year-end

$10 million – less than $20 million (Travel Retailer)

Annual: within 3 months; Quarterly: within 45 days after each quarter

🧾 What’s a Financial Statement?

A financial statement shows how healthy and stable a business is. It must include:

A statement of sales in Ontario

A balance sheet (what the company owns and owes)

An income statement (profit and loss summary)

A cash flow statement (money coming in and going out)

A reconciliation of trust accounts (how customer money is handled)

These statements must be prepared by a Licensed Public Accountant and accompanied by:

A review engagement report, or

An audit report (for larger businesses or as required under the Business Corporations Act)

💡 Review engagement vs. audit: Both are checks done by accountants to make sure the numbers are accurate. An audit provides a higher level of assurance than a review.

🧮 What’s a Verification Statement?

Smaller businesses with less than $2 million in annual sales can file a verification statement instead of full financial statements.

This form (available on the TICO website) must include:

Total assets and liabilities at year-end

Total revenue and expenses for the year

Any other information requested by TICO

The form must be signed and certified as accurate by:

The registrant (if an individual)

A director or officer (if a corporation)

A partner (if a partnership)

By signing, this person is legally confirming that the information is correct.

🕒 Filing Deadlines and Extensions

All financial or verification statements must be filed within 90 days of your fiscal year-end.

The Registrar can grant an extension, but it’s not automatic — it’s at their discretion.

⚠️ Tip for the Exam: The 90-day rule and who signs the verification statement are common test questions!

💵 What Counts as “Sales in Ontario”?

When calculating your sales volume, “Sales in Ontario” means:

For travel retailers: The total amount paid or payable to or through the retailer for all travel services sold in Ontario.

For travel wholesalers: The total amount paid or payable to or through the wholesaler for all travel services sold in Ontario.

This definition is important because your sales volume determines what kind of financial reporting TICO expects.

📘 Key Definitions

Licensed Public Accountant (LPA): A professional licensed under the Public Accounting Act, 2004 who can perform audits or review engagements.

🧠 Summary for Exam Prep

Here’s what you should remember:

All registrants must file either a financial statement or verification statement every year.

$2 million in annual Ontario sales is the main cutoff between verification and financial statement filing.

Deadlines: 90 days after year-end for annual reports; 45 days for quarterly/semi-annual reports.

Prepared by: Licensed Public Accountant (for financial statements).

Verification statements can only be used by smaller agencies under $2 million in sales.

Registrar extensions are possible but not guaranteed.

Financial and Record-Keeping Requirements

Running a travel business in Ontario means keeping your finances organized and transparent. The Travel Industry Council of Ontario (TICO) has specific financial reporting and record-keeping rules that every registrant must follow. These rules help ensure consumer protection and business accountability.

Let’s break down the key financial requirements you’ll need to understand for the TICO Supervisor/Manager Level Exam.

Every TICO-registered travel agency or wholesaler must file financial statements or verification statements every year. The type and frequency of filing depend on your annual sales volume.

Here’s a summary (from Table 8.1):

Sales Volume (Ontario)

Type of Registrant

Reporting Requirements

Filing Deadline

Less than $2 million

Retailer or Wholesaler

Verification Statement or Annual Financial Statements

If the Registrar believes your financial documents don’t give a full picture, they may request additional or consolidated financial documents.

Consolidated financial statements combine the results of:

All the entities under the registrant’s control, and

Any related subsidiary operations.

This helps TICO see the complete financial health of the business.

For example:

If your travel business owns another travel company, both may be combined into one financial report.

If you’re a corporation, you may also need to include financial data from major shareholders.

If TICO Suspects Financial Trouble

If the Registrar believes a business might be in financial difficulty, they can request a written statement of your working capital (or proof that you are exempt from that requirement).

The Registrar may also require that the financial statements or written confirmation be verified under oath (affidavit).

Understanding Working Capital (Section 8.2)

What Is Working Capital?

Working capital shows your business’s ability to pay its short-term debts as they come due. It’s a simple way to measure the financial health of a company.

Here’s the formula: Working Capital=Current Assets−Current Liabilities

In plain words —

Working capital is what’s left after you subtract what your business owes (liabilities) from what it owns (assets) in the short term.

Examples

Current Assets (can be turned into cash within one year): Cash, bank accounts, accounts receivable, and short-term investments like stocks or mutual funds.

Current Liabilities (must be paid within one year): Accounts payable, taxes payable, and short-term loans.

Positive working capital means your business can pay its bills easily — this is what TICO wants to see. Negative working capital means you owe more than you own in the short term — this signals risk.

Section 24 of the Regulation

Under Ontario’s Travel Industry Act, registrants must maintain positive working capital at all times. This ensures your business can meet its financial obligations and protects consumers who book travel through you.

However, not all assets count toward working capital. The following are excluded:

Security deposits from new applicants

Capital belonging to an “interested person” (like shareholders or related companies)

Intercompany receivables or payables (money owed between related businesses)

IATA deposits or credit card processor deposits

Who Is an “Interested Person”?

According to TICO’s definition, an interested person is someone who:

Has a beneficial interest in the business

Controls or influences the business directly or indirectly

Has provided or may provide financing to the business

In short, it’s anyone financially tied to your company who could affect its stability.

Exemptions to the Working Capital Requirement

Some organizations are exempt from maintaining positive working capital if they meet all of the following conditions:

The registrant is a not-for-profit corporation without share capital.

They have a transfer payment or funding agreement with:

The Ontario government (the Crown), or

A municipality.

The agreement is:

For at least one year,

Still in effect, and

Requires the organization to promote tourism in Ontario.

A copy of the agreement is filed with the Registrar.

Any requested additional information is provided within the specified time.

The registrant informs TICO of any changes to the agreement promptly.

These organizations are considered low-risk because they are government-funded and not-for-profit.

Key Takeaways for the Exam

✅ Businesses must file financial or verification statements every year — deadlines depend on sales volume. ✅ TICO can request extra or consolidated financial documents for clarity. ✅ All registrants must maintain positive working capital — assets > liabilities. ✅ Certain government-funded, non-profit organizations are exempt from working capital rules. ✅ The Registrar has the power to demand more documents or verification if financial concerns arise.

Pro Tip: For exam questions, remember this rule of thumb:

“The larger the sales volume, the more frequent and detailed the financial reporting required.”

8.3 Legal Responsibility for Deposits

Reference:Section 25 of the Travel Industry Act

When a travel agency or wholesaler (called a “registrant”) accepts money from a customer, they are legally responsible for that money.

In legal terms, they are “jointly and severally liable.” This means they can be held fully responsible for refunding or repaying customers, even if other parties were involved in handling the money.

However, a registrant does not have to refund the customer if all of these conditions are met:

💰 Money was properly disbursed — The agency paid the correct supplier or another registrant for the travel services.

🤝 Acted in good faith and at arm’s length — The agency acted honestly, fairly, and without close personal or financial ties influencing the decision.

🚫 Did not deal with illegal operators — The other party involved must also be legally registered under the Act.

If all three of these points are satisfied, the registrant is protected from being held liable for a customer refund.

Key Definitions to Remember

Jointly and Severally Liable — You’re legally responsible as both an individual and as part of a group.

Good Faith — Acting honestly and fairly, without the intent to cheat or deceive.

Arm’s Length — Doing business with someone who isn’t personally or financially connected to you.

These terms often appear in TICO exams — make sure you can recognize them and explain what they mean!

8.4 Trust Accounting

Reference:Sections 26 and 27 of the Regulation

Trust accounting is a consumer protection system that ensures customers’ money is kept safe until their travel services are provided.

Under this system, all money received from customers for travel must be placed in a separate bank account called a Trust Account. This money cannot be used for the business’s operating costs — only for paying suppliers, issuing refunds, or transferring earned commissions after the trip is completed.

Purpose of Trust Accounting

✅ Protect customers’ money if a travel agency goes bankrupt or insolvent. ✅ Allow TICO to monitor agencies’ financial health. ✅ Prevent agencies from using customer funds for business expenses.

Requirements for Setting Up a Trust Account

The account must be opened in an approved financial institution in Ontario, such as:

A Schedule I or II bank under the Bank Act (Canada)

A loan or trust corporation

A credit union under the Credit Unions and Caisses Populaires Act, 1994

The account must be in the legal business name of the registrant (for example, “DreamWorld Travel Inc.” and not “John Smith”).

The account must be clearly labeled as a “Travel Industry Act Trust Account.”

Any funds received from customers must be deposited within two banking days of receipt.

All registrants must have at least one trust account, unless exempt under specific conditions.

Two Main Accounts a Travel Agency Operates

🟩 Trust Account

This account holds all customer payments for travel services. Money in the trust account can only be used to:

Pay suppliers of travel services

Refund customers if needed

Transfer earned commission or markup after suppliers are fully paid or services are completed

Important: The money in the trust account cannot be used to pay rent, salaries, or office expenses.

🟦 General Account

This is the business operating account used for expenses like rent, utilities, and wages. Only after the travel services are completed and the supplier has been paid can commissions or markups be transferred from the trust account to the general account.

Clarifying “Money Received from Customers”

Section 26.1 of the Regulation defines what counts as “money received from customers for travel services.”

It includes any payment a registrant directly receives, but excludes:

Payments made through the registrant directly to the supplier’s merchant account (because the agency never handles the funds).

Payments for future services that are not due yet during that reporting period.

Example: If a customer pays a deposit today and their final payment is due next month, only the deposit counts as money “received” right now.

However — if the customer’s credit card payment goes through the agency’s merchant account, then that money is considered received and must be deposited into the trust account.

Quick Recap for Exam Prep

Term

Meaning

Key Point

Jointly and Severally Liable

Legally responsible both individually and as part of a group

Applies when registrants handle customer funds

Trust Account

Special account for holding customer payments

Money must stay there until services are completed

General Account

Business expense account

Used only after commissions can be transferred

Good Faith

Acting honestly and fairly

A key defense in liability cases

Arm’s Length

Unrelated, independent business dealings

Ensures fair transactions

In short: Trust accounting and financial responsibility protect consumers and ensure travel businesses stay compliant under Ontario’s Travel Industry Act, 2002. As a TICO supervisor or manager, you must understand how to handle customer deposits, maintain trust accounts, and meet all regulatory deadlines.

Understanding Security Instead of Trust Accounting

Chapter 8: Financial and Record-Keeping Requirements

When running a travel business, it’s important to protect customer money. Normally, travel agencies must keep customer payments for travel services in a trust account. However, if a business has proven financial stability, it can choose another option — providing a security deposit to TICO.

Let’s go through how this works, step-by-step.

What Does “Security Instead of Trust Accounting” Mean?

According to Section 28 of the Regulation, some registrants (travel agencies or wholesalers) can use a security deposit instead of maintaining a trust account.

Definition

In simple terms, the “money received from customers for travel services” means:

The money that the registrant actually gets from customers during a certain period.

It does not include:

Payments made directly by customers to another company through the registrant.

Travel sales that are made during that period but are paid for after the period ends.

Who Can Use a Security Deposit?

Only registrants who have been continuously in business for at least one fiscal year are allowed to use this option.

Instead of having a trust account, they must file a security deposit with TICO — for example:

A letter of credit

A bank draft

Collateral, like a GIC (Guaranteed Investment Certificate)

How Much Security Is Required?

The deposit amount must be equal to or greater than one-sixth (1/6) of all customer money received for travel services over the last 12 months.

The financial statements submitted to TICO must show:

The total amount of money received from customers for travel services during the reported period.

TICO must receive the security deposit within 30 days after the registrant files financial statements.

Note: The registrant must keep their trust account active until they get an official letter from TICO confirming that the security deposit has been accepted.

New Applicant Security Requirement

According to Section 25 of the Regulation, any new applicant (someone not registered in the past 12 months) must provide a $10,000 security deposit when applying to TICO.

TICO will return this deposit after:

The registrant has filed two complete and consecutive annual financial statements, showing financial stability, and

The Registrar has no concerns about compliance with the Travel Industry Act or its regulations.

If there are concerns, TICO may hold the $10,000 until those issues are resolved. New registrants must also operate both a trust account and a general account.

What If the Business Closes or Goes Bankrupt?

If a registrant with a security deposit becomes bankrupt, insolvent, or closes down, TICO will return the security after at least six months. However, any amount used to pay customer claims will be deducted before the security is returned.

Exemption for Low-Risk Tourism Businesses

Some lower-risk organizations may not need to file a security deposit. To qualify for this exemption, the following must be true:

The registrant is a not-for-profit corporation without share capital.

It has a funding agreement (e.g., transfer payment agreement) with:

The Ontario government, or

A municipality.

The agreement:

Has a term of at least one year.

Has not expired.

States that the registrant’s purpose is to promote tourism in a specific area of Ontario.

A copy of the agreement is provided to the Registrar.

The registrant provides any additional information requested by the Registrar.

The registrant notifies TICO in writing of any changes or amendments to the agreement.

If the agreement is with a municipality, two more conditions apply:

The municipality must have a financial arrangement with TICO (e.g., guarantee or indemnity).

The Registrar must confirm in writing that this condition is satisfied.

If the Registrant Stops Qualifying for the Exemption

If a registrant loses its exemption, what happens depends on timing:

1. Before Two Annual Statements Filed

They must immediately provide $10,000 in security to TICO.

2. After Two Annual Statements Filed

They must notify TICO in writing as soon as possible. After receiving the notice, the Registrar will:

Confirm if there are no compliance concerns, or

Set a deadline to provide the $10,000 security deposit, or

Specify any repayment amounts needed for claims that may be made from the Compensation Fund (up to $10,000).

If the registrant already has an approved municipality financial arrangement with TICO, no further action is needed.

When and How Security Is Returned

Once the registrant has filed two full annual financial statements, and there are no outstanding compliance issues, TICO will return the security.

If TICO has paid out or expects to pay out any claims related to:

Bankruptcy,

Insolvency, or

Business closure,

then those amounts will be deducted from the returned security.

🧠 Key Points to Remember for the TICO Exam

Trust account or security — Registrants must protect customer money either way.

Security amount = 1/6 of last year’s customer payments.

New applicants → Must pay $10,000 security.

Exemptions exist for government-linked not-for-profits.

Security is returned only after two full financial years of compliance.

8.6 Record-Keeping

Reference: Section 29 of the Regulation

Every TICO-registered business must keep accurate and complete business records. These records are important for accounting, audits, and ensuring compliance with the Travel Industry Act.

📘 Key Rules for Record-Keeping

All business records must be kept at the main office (principal place of business) or another location approved in writing by the Registrar.

Records must be kept for at least six years after the date of the transaction.

🧾 Types of Records You Must Keep

Accounting records – These should detail your business income and expenses. You must include all supporting evidence such as:

Invoices

Statements

Receipts (each with a unique serial or reference number)

Banking records – These must show all financial transactions linked to your business.

Payment records – Keep written records of all money paid to or from your business for travel services. Each transaction must be easy to identify by a unique number or code.

Refund or alternative service records – If you offer customers refunds or alternative travel services due to changes in plans, you must keep a file showing:

What happened

What action your business took

Whether the customer accepted the alternative or refund

All these records must be available for inspection by the Registrar at any time.

8.7 Financial Inspection Program

TICO uses a risk-based financial inspection program to make sure all registrants are financially stable and following the law. This helps protect consumers and keeps the travel industry trustworthy.

🔍 Why TICO Inspects Financial Records

TICO staff check whether:

Financial statements are filed on time

Businesses maintain enough working capital

Trust accounts are properly set up and used

If a registrant fails to meet these standards, TICO may issue warning letters or even propose to revoke the registration.

🔹 The Financial Inspection Program Has Two Main Parts:

1. Financial Statement / Document Bench Review

Once a registrant’s financial statements are submitted, a TICO financial inspector (usually a CPA) reviews them.

During this bench review, the inspector looks at:

Sales

Working capital

Profit or loss

The goal is to check if the business meets the working capital and trust account requirements of the Regulation.

2. Site Inspection

If TICO suspects potential problems—like weak financial health, improper trust account use, or repeated losses—a site inspection is conducted.

During this visit, a financial inspector:

Reviews the registrant’s records in detail

Determines if there is a compliance issue

Prepares a full Inspection Report for the Registrar

🚨 Other Reasons for Site Inspections

Site inspections can also happen if:

Consumers or other registrants file complaints

TICO staff notice red flags during reviews

The registrant is a new business (all new registrants are inspected within their first year)

TICO monitors all registrants regularly and follows up on any non-compliance issues.

Registrar’s Requests for Further Information

After reviewing the Inspection Report, the Registrar may ask for more details.

Here’s what might be required:

Written Statement of Current Working Capital

If the Registrar believes a business might be in financial trouble, they can ask for a written and verified (by affidavit) statement of working capital.

Exemption from Working Capital Requirement

Businesses that qualify for an exemption must still provide a written statement confirming that they meet the exemption criteria.

Audited Financial Statements

The Registrar can request audited and consolidated financial statements (including related businesses or shareholders) if needed for a complete review.

Why Compliance Matters

The goal of TICO’s inspection staff is to help registrants comply, not to punish them unnecessarily.

If a business fails to meet working capital or trust account requirements, TICO will:

Notify the registrant

Give them time to fix the problem

However, if the issue isn’t corrected, TICO can take administrative action—including the revocation of registration.

So, registrants should always resolve financial issues quickly to prevent them from escalating into serious problems.

✅ Chapter Summary

By the end of this chapter, you should understand:

How to properly keep and store financial records

How TICO monitors financial compliance through inspections

What happens if your business fails to meet financial standards

The importance of maintaining transparency and cooperation with TICO

📘 Study Tip:

TICO exam questions from this chapter often focus on:

How long records must be kept

What documents are included in record-keeping

What triggers a site inspection

How TICO handles non-compliance

🧠 Quiz Reminder

You’ve completed Chapter 8: Financial and Record-Keeping Requirements! Log into your MyTICO account and try the Chapter 8 quiz to test your understanding. You’ll get instant feedback — and remember, you can take the quiz as many times as you like.

TICO Registration Requirements: A Simple Study Guide

If you want to work in the travel industry in Ontario at a supervisor or manager level, you must understand who needs to register with TICO and who is exempt. This chapter breaks it down so you can easily learn it for your exam.

Let’s go step-by-step.

7.1 Who Must Be Registered

Any travel retailer or travel wholesaler that wants to sell travel services in Ontario must be registered with TICO.

This includes:

Travel agencies (physical offices or online websites)

Travel wholesalers (companies that package travel services and sell them to agencies)

Individuals operating as a travel business (sole proprietors, partnerships, or corporations)

If you sell travel services in Ontario and are not registered with TICO — it’s illegal.

Any services combined with transportation or accommodation (like packaged tours)

Anyone legally registered is called a registrant.

✅ Individual registrants must live in Canada ❌ TICO registration is not transferable

Exemptions — Who Doesn’t Need to Register?

Some groups and companies do not need to register with TICO. These rules come from Section 2 of the Regulation.

Important for exam: If a business is exempt and not registered with TICO, the Travel Industry Compensation Fund DOES NOT protect consumers booking with them.

Here are the main exemptions:

Companies Not Required to Register

Type of Company

Explanation

Travel retailers/wholesalers not located in Ontario

If the company is outside Ontario, they don’t need TICO registration even if Ontarians book with them

Companies advertising to Ontarians (online, toll-free phones) but located elsewhere

Example: Out-of-province online travel agency

End suppliers

Airlines, cruise lines, hotels, car rental companies

End Suppliers Offering Local Services

Exempt Group

Key Points

End supplier offering local services (within 25 km)

Example: a hotel offering accommodation + local theatre tickets + transport

End supplier adding services from another company (not airline/cruise/bus)

Must collect no more than 25% upfront or payment no more than 30 days in advance

Purpose: Help small local tourism businesses operate without heavy regulation.

Public Carriers & Their Agents

Exempt Group

Example

Public carrier selling scheduled transportation

Bus service from New York to Toronto 4 times/day

Agents selling for a public carrier

Ticket booth selling bus tickets

Real Estate Professionals (Short-Term Rentals)

Real estate brokers, salespersons, and brokerages do not need TICO registration IF:

They are registered under the Real Estate and Business Brokers Act, 2002

They ONLY handle short-term rental accommodations through their brokerage

They DO need TICO registration if:

They do it as a side business outside their brokerage

They also sell transportation or tickets to attractions

One-Day Tour Providers

Exempt ONLY IF:

They sell one-day tours ONLY

The tour starts and returns within 24 hours

No accommodation included

Examples: One-day bus trips to 🎭 theatre | 🎰 casino | ⚽ sports game | 🎿 ski hill | 🛍️ shopping mall

NOT exempt if: They also offer overnight tours

Guide or Sightseeing Services

Exempt if:

They only sell guide services

They do NOT provide transportation or accommodation

Example: A tour guide showing visitors around local landmarks on foot.

Educational Institutions

Schools are exempt if:

The teacher arranging the trip works at the school

The trip is approved by the school board or principal

Teacher receives no profit

One-day student field trips (ex: Royal Ontario Museum)

Religious Groups, Amateur Sports Teams, Associations

(Overland Travel Only)

Exempt IF ALL conditions are met:

Only members can join the trip

Purpose is educational, cultural, religious, or athletic

Funds kept in a trust account

No one profits except by participating in the trip

Destination within 2,000 km

Transportation vehicle stays at destination (ensures return)

Not-For-Profit Clubs

(Overland Travel Only — Same rules as above)

These clubs are also exempt under the same conditions — only members, no profit, trust account, within 2,000 km, bus stays at location.

Key Exam Takeaways

✅ Anyone selling travel services in Ontario must register with TICO ✅ Exempt groups are very specific — memorize them ✅ The Travel Compensation Fund only protects bookings through registered companies ✅ One-day tours = exempt (only if zero overnight trips) ✅ Schools, churches, sports teams = exempt under strict rules ✅ Real estate professionals exempt only for short-term rentals through brokerage ✅ End suppliers like airlines never need TICO registration

Final Study Tip

When studying exemptions, always ask yourself:

Does the business sell transportation or accommodation to the public in Ontario?

If YES → likely must register with TICO If NO → check if they fit one of the special exemption cases

TICO Registration Guide: Requirements to Become and Stay Registered

If you want to run or manage a travel business in Ontario, you must be registered with TICO. This chapter explains what you need to qualify and how to keep your registration active.

Think of this as a checklist to help you pass the TICO Supervisor/Manager exam.

7.2 Requirements to Become Registered

Before TICO approves someone to operate as a travel retailer or wholesaler, they must meet certain rules (Section 5 of the Regulation).

✅ Basic Requirements

To become registered:

If you are an individual:

You must be at least 18 years old

You must be a Canadian resident

✅ If You Were Previously Registered With TICO

TICO will check your history. You can only register if:

Requirement

What It Means

You do not owe the Travel Industry Compensation Fund

If you owe money, you must set up a payment plan TICO accepts

TICO has no unpaid judgments against you

If they do, you must settle it or have a payment plan

TICO never had to pay claims for you due to bankruptcy/closing your business

If they paid, you must reimburse TICO for claims & costs or have a repayment plan

✅ Security Requirement

If TICO requires you to provide security money (a financial guarantee), you must do so.

✅ Other People Connected to the Business

Anyone considered an “interested person” (owners, partners, certain directors — see Glossary in the Act) must meet the same rules.

Example: If you and your business partner apply, both of you must meet these conditions.

7.3 Requirements for Registration Renewals

Registration is not a one-time thing — you must renew and continue meeting requirements (Section 6).

To stay registered, a business must:

Be a resident of Canada if it’s an individual

Not owe any Compensation Fund payments (or have an approved payment plan)

Have no unpaid TICO judgments (or have a payment plan)

Have repaid any Compensation Fund claims TICO paid on their behalf (or have a repayment plan)

Provide security if required

You must stay in good standing with TICO at all times.

Forms & Fees — How to Register and Renew

(Section 3 of the Regulation)

To register as a travel retailer or wholesaler, you must:

✅ Fill out the registration form

✅ Submit it to TICO with the required fee

✅ Pay renewal fees every year online

✅ Register each branch office separately

✅ Pay branch fees online

Fee Structure

TICO sets registration and renewal fees

Fees are published in a Fee Schedule

Any fee changes must be:

Discussed with the industry, and

Approved by the TICO Board

Application Rules

Applications and renewals must:

Be submitted on TICO-approved forms

Include all required information

Be sent with correct payment

If anything is missing → TICO will NOT process the application.

Key Exam Takeaways

Topic

Memory Tip

Age & Residency

Individual must be 18+ and live in Canada

Debt to TICO?

Must pay or have a payment plan

Past bankruptcy claims?

Must reimburse TICO

Security deposit?

Provide if required

Renew every year

Online, with proper forms and fees

Branches

Must be registered one-by-one

Study Shortcut

Think of it like getting and keeping a driver’s license for your travel business:

Like Driver’s License

TICO Equivalent

You must meet eligibility rules

Age, residency, no debts/judgments

You must renew it

Annual registration renewal

You must follow rules or lose it

Must remain in good standing with TICO

TICO Registration Fee Guide: What You Need to Pay

To run a travel agency or a travel wholesaler business in Ontario, you must be registered with TICO. This chapter explains the fees you need to pay when registering and renewing your registration.

These rules come from Section 3(1) of Ontario Regulation 26/05.

✅ Fee Schedule effective since July 1, 2011 ✅ All fees cover a 1-year period

Let’s make it simple.

Registration Fees (When You First Sign Up)

When you first register with TICO, you pay a fee based on whether you are registering a head office or a branch office.

Type of Business Location

Fee

Travel Agency or Travel Wholesaler — Head Office

$3,000

Travel Agency or Travel Wholesaler — Branch Office

$800

❗ Registration fees are NOT refundable, even if your application is not approved.

Renewal Fees (Every Year)

Every year, travel agencies and wholesalers must renew their registration.

The renewal fee depends on your Ontario sales volume from the previous fiscal year.

Sales-Based Renewal Fees

Ontario Sales Volume

Renewal Fee

$2,000,000 or less

$300

More than $2,000,000 up to $5,000,000

$600

More than $5,000,000 up to $10,000,000

$900

More than $10,000,000 up to $50,000,000

$1,200

Over $50,000,000

$1,800

Branch Renewal Fee

If you have branch offices, each branch must pay:

Fee Type

Fee

Branch Office Renewal

$300 per branch

Important Renewal Timeline Rules

Renewal fees are due 90 days after the registrant’s year-end

Branch renewal dates match the head office renewal date

This means everything renews at the same time

Head office + all branches in one cycle

✅ Key Points to Remember for Your Exam

$3,000 to register a head office

$800 to register a branch

Renewal fees depend on sales volume

Branch renewal fee = $300 each

Fees must be paid every year

Fees are not refundable

Branches renew at the same time as head office

Renewal payment due 90 days after year-end

🎯 Quick Memory Trick

Term

Trick

Initial registration = Big money

$3,000 = Start-up cost for main office

Branches always cost

$800 to start, $300 yearly

Bigger sales = Bigger renewal fee

The more you sell, the more you pay

Everything aligned

Branches renew with head office

TICO Requirements to Become Registered – Part 2

To operate a travel business in Ontario, you must follow TICO rules. This part of the chapter covers security deposits, office rules, and business name rules.

Study this carefully — questions from this section often appear on the TICO Supervisor/Manager exam.

7.4 Security Deposit for New Applicants

Section 25 of the Regulation

When a business applies to register with TICO and has not been registered in the last 12 months, they must give TICO a security deposit of $10,000.

✅ Key Points

New applicants must provide $10,000 security

This applies only if the business was not registered in the past 12 months

The money is held by TICO

It will not be returned until:

The business submits two years of financial statements

The Registrar decides the business is in good standing and following the rules

The Registrar has the final say on returning the deposit.

🔹 Exemptions

Some low-risk tourism businesses tied to government may not need to pay this deposit. Details are found in Chapter 8 (Financial & Record-Keeping Requirements).

7.5 Requirements for Operating From an Office or Home

Section 6 of the Act + Sections 10 & 11 of the Regulation

All travel registrants must work from the location listed in their TICO registration.

✅ Office Rules

You can only operate from the address on your registration

If you have more than one location:

One must be the head office

All others must be registered branch offices

✅ Home-Based Travel Agencies

You can run a travel business from home, but only if:

Requirement

Meaning

Zoning approval

Local zoning must allow business activity

Separate business phone

Business phone number must be different from personal/home number

Record access

Registrar must be able to see your business records

If the Registrar can’t access your records, you cannot operate from home.

7.6 Business Name Requirements

Section 9 of the Regulation

Every travel agency must have a legally registered business name with ServiceOntario.

✅ Business Name Rules

You must register your business name

You must do business under the same name

Your name cannot pretend to be sponsored or affiliated with another company unless you truly are

❌ Examples of names NOT allowed

“Disney Travel” (unless you are actually approved by Disney)

“Air Canada Vacations Center” (unless you are authorized)

You cannot mislead customers into thinking you are connected to another travel brand.

🧠 Exam Tips

Topic

What to remember

Security deposit

$10,000 for new applicants; held for at least 2 years

Home office

Must follow zoning, have separate phone, and records accessible

Business name

Must be legally registered & not imply fake partnerships

🎯 Quick Memory Trick

Rule

Shortcut

Security

$10K trust test — 2 years, must be in good standing

Home office

Zoning + phone + records

Business name

Register name + no fake partnerships

Requirements to Become and Stay Registered with TICO

When you run or supervise a travel business in Ontario, you must follow TICO rules. These rules protect consumers and make sure only honest and qualified businesses sell travel services.

This chapter covers important rules about TICO registration and how to keep your registration active.

Certificate of Registration (Section 13 of the Regulation)

After you complete the TICO registration process, TICO gives your business a Certificate of Registration.

Key Points to Remember

The certificate must be kept at the office or branch location it belongs to.

Anyone can ask to see it — you must be able to show it.

Best practice: display the certificate in your office for customers to see.

The certificate has an expiry date — make sure it stays valid.

If Your Business Closes or Registration Ends

If your business:

shuts down,

loses registration,

or gets suspended,

you must return the certificate to TICO immediately — either by registered mail or by hand.

Exam Tip ✅

If a TICO-registered business closes, they must return the Registration Certificate right away.

Requirements to Maintain Registered Status

Even after you register, you must continue following all TICO rules. If you don’t, TICO can refuse renewal or cancel your registration.

When TICO Can Refuse Registration or Renewal

TICO may say no if:

The business is not financially responsible.

There is proven dishonesty.

The business breaks the Act or Regulation.

The business does not provide information TICO asks for.

Rules for Selling Travel Services (Section 12 of the Regulation)

Travel retailers must follow these rules when selling travel services:

1. Tell Customers Who You Are

You must give customers:

your business name,

office address,

and phone number.

This helps the customer know exactly who they are dealing with.

2. Disclose Relationships

If your agency is connected to a travel wholesaler (for example, the wholesaler owns the travel agency), you must tell the customer.

3. Only Registered People Can Sell Travel

Travel services can only be sold by:

a registered business, and

individuals employed by or contracted with that business.

4. Everyone Selling Travel Must Pass Exams

Anyone who sells travel or advises the public must:

Pass the Travel Counsellor Exam

If they become a supervisor/manager, they must also pass the Supervisor/Manager Exam within 6 months

Educational Requirements (Sections 15–16 of the Regulation)

Every travel office must have a qualified supervisor/manager.

Supervisor/Manager Requirements

They must:

Pass the Travel Counsellor Exam

Have sufficient experience (usually 3 years of selling travel)

Pass the Supervisor/Manager Exam – Either already passed, or must pass within 6 months of taking the role

Requirements for All Travel Counsellors

Anyone selling travel to the public must:

Pass the Travel Counsellor Exam

Be an employee or contracted person with the agency

Have their training records and certificates kept on file by the registrant

Notification of Changes

Registrants must inform TICO when key business information changes, including:

business ownership

partners or shareholders

office location/address

bank accounts

supervisor/manager

Some changes need advance approval; others just need to be reported on time.

Exam Tip ✅

Any major change to the business must be reported to TICO within required timelines — some changes need pre-approval.

Simple Summary

Requirement

Key Rule

Certificate of Registration

Keep it at the office, show it when asked, return if business closes

Selling Travel

Only by registrants and approved individuals

Education

Travel Counsellor Exam for sellers; Supervisor exam within 6 months

Supervisor/Manager

3 years experience + required exams

Change Reporting

Must notify TICO about major business changes

Final Exam Checklist ✅

Before moving on, make sure you remember:

Where the Registration Certificate must be kept

When it needs to be returned

Who can sell travel services

The exam requirement timelines

Supervisor/manager experience and exam rules

That major business changes must be reported to TICO

If you can explain all of these in simple terms, you’re ready for questions on this chapter!

🧠 Chapter: Requirements to Become (and Stay) Registered with TICO

📜 7.7 Certificate of Registration

Once a business completes the TICO registration process, TICO gives them a Registration Certificate.

Important things to remember:

The certificate must be kept at the office or branch it belongs to

It must be shown to anyone who asks

Best practice: display it clearly where customers can see it

The certificate has an expiry date — registration must be renewed

If the business closes, is suspended, or revoked, the certificate must be returned to TICO immediately (by registered mail or in person)

💡 Exam Tip: TICO encourages consumers to look for this certificate before booking travel — it’s proof the company is legally registered.

🔐 7.8 Requirements to Maintain Registered Status

Even after registration, businesses must follow rules to stay registered.

🚫 When can the Registrar refuse or revoke registration?

The Registrar can refuse or cancel registration if the business or person:

Lacks financial responsibility

Has acted dishonestly

Breaks laws or TICO rules

Refuses to provide required information

In short: you must be financially stable, honest, and cooperative.

Tell customers the business name, address, and phone number

Tell customers if the retailer is connected to another travel business (example: a wholesaler that owns a travel agency)

Only sell through:

A registered travel business, and

People employed by or contracted with that business

Ensure everyone selling travel or giving advice has passed the Travel Counsellor Exam

Ensure new supervisors/managers pass the Supervisor/Manager Exam within 6 months

🎓 Education Requirements (Sections 15–16)

Each travel office must have a supervisor/manager who:

✅ Has passed the Travel Counsellor Exam ✅ Has minimum 3 years travel-selling experience (common interpretation of “sufficient experience”) ✅ Is approved by the Registrar ✅ Has passed the Supervisor/Manager Exam OR will pass it within 6 months of starting

Also:

Everyone selling travel to the public must pass the Travel Counsellor Exam

Travel counsellors must be employees or contracted

The business must keep proof of education certificates

💡 Exam Tip: Remember: 3 years experience + Travel Counsellor Exam + Supervisor/Manager Exam within 6 months.

🔔 Notification of Changes — What to Report & When

Registrants must tell TICO about business changes. Some need approval, some just need notification.

Type of Change

Approval or Notice?

Time to Report

Changes to officers/directors (corporation) or partners

Registrar Approval

Within 5 days

Someone gets 10% or more shares or increases share beyond 10%

Notify Registrar

Within 30 days

Change of business address

Notify Registrar

5 days in advance

Change in supervisor/manager

Notify Registrar

5 days in advance (or immediately if unexpected)

Change in bank account details

Notify Registrar

5 days in advance

Any other change in registration info

Notify Registrar

Within 5 days

Ceases selling travel services

Notify Registrar

ASAP (or at least 10 days in advance if known)

Stops trading with another registrant due to financial concerns

Notify Registrar

Promptly

Change in address for service

Notify Registrar

Within 5 days

💡 Exam Tip: 5 days & 30 days deadlines are common — expect them on the test.

📝 Summary for Exam Success

To stay registered with TICO, a travel business must:

Display its Registration Certificate

Operate honestly and financially responsibly

Ensure all staff selling travel are certified

Have a qualified Supervisor/Manager

Report business changes on time

Requirements to Become Registered — Part 3

Compliance, Inspections, Refusals & Revocations)

When running a travel business in Ontario, being registered with TICO is not a “one-and-done” thing. You must follow rules to protect consumers and keep your license active.

This chapter explains compliance, inspections, and how registrations can be refused, suspended, or revoked.

✅ 7.9 Compliance — What It Means and Why It Matters

When consumers book with a TICO-registered travel agency or website, they are protected. For example, they may be able to claim money from the Travel Industry Compensation Fund if a registered agency or supplier (like an airline or cruise line) goes bankrupt.

What TICO Does to Enforce Compliance

TICO has a Compliance Department that checks if businesses follow the law.

They monitor:

Type

Focus

Financial compliance

Financial statements, trust accounting, working capital

Non-financial compliance

Advertising, invoices, disclosures, and unregistered sellers

TICO reviews ads, websites, brochures, and responds to consumer and industry complaints.

Selling travel without TICO registration is illegal. TICO can charge offenders.

What Happens if a Business Breaks the Rules?

TICO contacts the registrant and asks them to fix the problem

The business must respond fast — not responding = non-compliance

If not corrected, the Registrar may move to revoke registration

Key Exam Reminder

If a registrant ignores TICO or refuses to fix compliance issues, their license is at risk.

🕵️ 7.10 Inspections — What to Expect

Section 17 of the Act

TICO can conduct inspections to make sure rules are being followed.

Inspectors Can:

Enter the business premises at a reasonable time

Ask to see records, documents, and bank info

Copy or take records as long as they give a written list

Investigate complaints

Your Rights

You may ask the inspector to show proof that they are authorized.

Your Obligations

You must NOT:

Block the inspector

Hide, change, or destroy documents

Doing so is an offence.

❌ 7.11 Refusal, Suspension, or Revocation of Registration

If a business does not follow the law, the Registrar can propose to:

Refuse registration

Suspend registration

Revoke registration

Refuse renewal

Add conditions to registration

The business must be notified in writing and has the right to appeal to the Licence Appeal Tribunal.

🚫 Refusal to Register — Common Reasons

Registration may be refused if:

Applicant has a serious criminal record

Applicant is not financially responsible

False information was given in the application

⚠️ Immediate Suspension

In serious cases, where consumers are at risk, the Registrar can suspend immediately.

This usually happens when there are major financial issues that could harm the public.

Suspension takes effect instantly

Must be in the public interest

Expires after 15 days unless extended by the Tribunal

❌ Revocation — Common Reasons

A registration may be revoked if the registrant:

Fails to file financial statements

Has trust account or working capital deficiencies

Does not pay Compensation Fund fees

Uses false or misleading advertising

Has invoicing issues

Has unresolved consumer complaints

Fails to respond to TICO

Shows ongoing dishonesty or non-compliance

Repeated violations can lead to revocation.

🔍 Public Access to Information

TICO can publicly share:

Names of registrants

Registration status

Business contact details

Charges or violations

Tribunal decisions

This makes the system transparent and protects consumers.

🎯 Exam Takeaways

Remember these key points:

💡 TICO enforces both financial and non-financial compliance 💡 Ignoring TICO letters = non-compliance 💡 Inspectors can access records and must not be obstructed 💡 Registration can be refused, suspended, or revoked 💡 Businesses have the right to appeal to the Licence Appeal Tribunal 💡 TICO can publish info about registrants to the public

In this chapter, we’ll cover what happens when there are issues with TICO registration — like appeals, offences, and confidentiality rules. As a future travel industry manager, you must understand how TICO enforces the law and protects consumers.

This info is important for your exam — so read carefully!

🚨 7.12 Appeals to the Licence Appeal Tribunal (LAT)

If TICO refuses, suspends, or revokes a company’s registration, the business has the right to appeal the decision to the Licence Appeal Tribunal (LAT).

What is the Licence Appeal Tribunal?

An independent tribunal (like a court but simpler and faster)

Handles TICO appeals

Members include legal, industry, and consumer experts

When can someone appeal?

New applicants who are refused registration

Current registrants whose registration is suspended or revoked

How to appeal

Must send a Notice of Appeal within 15 days

There is a non-refundable fee

You may represent yourself or hire a lawyer/paralegal (your expense)

If no appeal is requested, the Registrar’s decision stands

What happens in a hearing?

Registrar and applicant/registrant present evidence

Tribunal makes a written decision

They can:

Confirm TICO’s decision

Overturn it

Add conditions to the registration

Can issues be solved before the hearing?

Yes. TICO often works with businesses to fix problems even after the appeal is filed. Example: Agreeing to follow extra rules to keep registration.

🔁 Re-Applying After Being Refused or Revoked

If TICO refuses or revokes a registration:

Must wait at least 30 days before re-applying

Cannot operate during this period

Must prove circumstances have changed and requirements are now met

⚖️ 7.13 Offences Under the Act

Once a business is registered, it must follow all TICO laws. If someone breaks the rules, it’s an offence.

What counts as an offence?

Giving false information

Not following the law or regulations

Who is responsible?

The business

Officers/directors — they must take reasonable care to prevent offences

Penalties

Offence

Maximum Penalty

Individual

$50,000 fine, up to 2 years minus a day in jail, or both

Corporation

$250,000 fine

Other consequences

Court can order restitution (money paid back)

Case must start within 2 years of TICO learning about the offence

🔒 7.14 Confidentiality

TICO handles private business info. This information must stay confidential except when allowed by law.

When can TICO share information?

When needed to enforce the Act

With consumer protection agencies

With law enforcement

With a person’s legal advisor

If the person gives consent

Important note

TICO staff cannot be forced to testify in civil court about confidential info — unless it’s a case under the Travel Industry Act.

✅ Chapter Complete!

You have finished Chapter 7 — Registration Requirements.

💡 Tip for your exam: Focus on appeals timelines, penalties, and confidentiality rules — these often show up in questions.

📌 Go back to your MyTICO portal and take the voluntary Chapter Quiz. You can try as many times as you want — quizzes don’t affect your final exam score but help you practice!

👨👩👧👦 Case Study: The Nicholson Family — Typical Canadian Family with University Kids

Understanding a typical family scenario is crucial for new tax preparers. Families with children in post-secondary education often qualify for multiple tax credits, deductions, and special considerations. This guide walks you through how to prepare a complete tax return for a family like the Nicholsons, including step-by-step instructions in Intuit ProFile, explained for absolute beginners.

🎯 Meet the Nicholson Family

Family Composition:

Parents: Scott (self-employed, dividend income) and Tracy (HR professional)

Children: Four children

Melissa (adult, university student)

David (adult, trades student)

Twins (young children, 6 years old in this scenario)

Key Family Details:

Scott is self-employed and receives dividends instead of a salary.

Tracy lost her corporate job mid-year, received a severance package, and quickly found a new position.

Family has recently become homeowners and may be eligible for first-time homebuyer benefits.

Children are enrolled in post-secondary programs or require childcare and summer camp deductions.

💰 Income & Deductions Overview

Scott (Self-Employed, Dividend Income):

Receives monthly dividends ($8,000/month)

Makes a year-end tax installment ($20,000) instead of monthly

ProFile Tip: Enter dividend income under the T5 slips section → the software will automatically calculate gross-up and dividend tax credit

Tracy (Employment & Severance):

Employment income reported on T4 slips

Severance included in T4 (plus any legal settlement received after year-end)

Professional dues ($585.75) and certification fees are deductible

ProFile Tip:

Enter employment income on T4 slips section

Enter deductions under “Professional Memberships & Dues” and “Employment Expenses” if applicable

🎓 Tuition and Education Credits

Melissa & David (Post-Secondary Students):

Tuition paid: Melissa ($11,252), David (amount based on T2202)

Eligible for tuition tax credits, which can be:

Applied to student’s own tax return

Transferred to parents if the student does not need full credit

ProFile Tip:

Use T2202 section → enter tuition paid for each student

Select the parent who earned income and will claim deduction

🏡 Homeownership Considerations

Family recently purchased their first home

Eligible for First-Time Home Buyers’ Tax Credit (HBTC)

ProFile Tip:

Enter purchase information under Home Buyers’ Amount

Software calculates credit automatically

💡 Notes for New Tax Preparers

Installments vs. regular tax payments:

Scott made a year-end installment, which may generate a small interest adjustment. ProFile handles CRA interest calculation automatically if installment info is entered.

Severance and legal settlements:

Include in income in the year received

If settlement crosses years, enter the date received to ensure proper reporting

Tuition and education credits:

Keep all T2202 slips for CRA verification

Transfer unused credits to parents if students don’t owe enough tax

Childcare & summer camp:

Only the parent with earned income can claim childcare deduction

Ensure receipts and amounts match CRA requirements

💻 How to Prepare in Intuit ProFile (Step-by-Step Beginner Guide)

Enter Personal Information:

Parent and children details, SIN, dates of birth

Enter Income:

Scott’s T5 slips → dividend income

Tracy’s T4 slips → employment and severance

Deductions & Credits:

Professional dues and certification fees

Tuition and education credits (T2202)

Childcare and summer camp expenses

First-Time Home Buyers’ Amount

Apply Transfers:

Tuition transfer to parents if applicable

Finalize Tax Return:

Review all CRA-required slips

ProFile auto-calculates total income, deductions, and credits

Check summary page for refund or balance owing

🌟 Key Takeaways

✅ Families with post-secondary children have multiple tax credits available ✅ First-time homebuyer credit is important to include ✅ Childcare expenses must be claimed by parent with earned income ✅ Tuition can be transferred to parents for maximum benefit ✅ ProFile automates calculations but accurate input is crucial

This case study of the Nicholson family is a perfect beginner-friendly reference for tax preparers handling typical Canadian families, showing how to maximize credits, properly report income, and navigate Intuit ProFile step by step.

💻 Case Study: Entering Income & Deductions for Scott and Tracy Nicholson

When preparing a tax return for a typical family with post-secondary children, understanding how to enter income and deductions correctly is essential. This guide walks through the Nicholson family scenario, showing beginner-friendly steps in Intuit ProFile and explaining key considerations for each type of income and deduction.

🧾 Overview of the Nicholson Family

Scott and Tracy Nicholson are a typical family with:

Two adult children in university (Melissa and David)

Two younger twins requiring child care

Scott is self-employed and receives dividends from his own corporation