Table of Contents

- 📘 Introduction to the Filing and Administrative Process for Dividends

- 🏛 Review the Classes of Shares to Ensure Dividends Can Be Paid

- 📊 Calculations May Be Necessary to Determine Per Share Dividend Amounts

- ⚖️ Consider the New Rules for Paying Dividends – The Over-Arching Principle (TOSI Explained)

- 🚂 TOSI – Weaving Through the Complexities of the New Rules

- 🚂 Getting Off the TOSI Train and Meeting an Exception

- 🚪 What Are the Exceptions and Excluded Amounts to TOSI?

- 📊 Quick Reference Chart & CRA Resources to Help You Navigate the Complex TOSI Rules

- 👷 Excluded Business Test for Active Involvement in the Business

- 💰 Reasonable Return Test for Reasonable Return on Capital Put Into the Business

- 🏢 Excluded Shares Test for Non-Service Related Business Corporations

- 📜 Letter to Lawyer to Update the Minute Book (Dividend Declaration Guide)

- ⚖️ Can Accountants Do the Minute Book Update as Part of Their Practice?

- 📊 How Frequently Should You Declare and Pay Dividends? (For Corporate Owner-Managers)

- 💰 Are There Any Remittances for Dividends? (Personal Tax Payment Implications)

- 🧾 Choosing to Pay Eligible or Ineligible Dividends

- 📄 Preparing and Filing the Year-End T5 Slip and Summary for Dividends Paid

- 🧓 Instructing or Helping Clients Determine Their Current CPP Status

📘 Introduction to the Filing and Administrative Process for Dividends

When working with corporate owner-managers, compensation does not always come in the form of salary.

The second major compensation method is:

💰 Dividends

Dividends can be tax-efficient — but they require proper legal documentation, tax compliance, and administrative discipline.

As a tax preparer, you must understand:

- How dividends are declared

- What documents are required

- How they are reported

- When special tax rules apply

- What filings must be completed

This section builds the foundation.

💡 What Is a Dividend?

A dividend is a distribution of after-tax corporate profits to shareholders.

Unlike salary:

- ❌ No CPP contributions

- ❌ No EI deductions

- ❌ No payroll remittances

- ❌ No T4 slip

Instead:

- ✅ Reported on a T5 slip

- ✅ Taxed personally as dividend income

- ✅ Subject to dividend tax credit rules

Dividends are investment income — not employment income.

⚖️ Salary vs Dividend — Administrative Comparison

Salary

- Payroll account required

- Monthly remittances to the Canada Revenue Agency

- T4 issued

- CPP applies

- Creates RRSP room

Dividend

- No payroll account

- No CPP

- No RRSP room generated

- Requires corporate resolution

- T5 issued

Different income types require completely different compliance processes.

🏛 Dividends Must Be Properly Declared

This is where many beginners make mistakes.

Dividends cannot simply be “taken out” of the company.

They must be:

- 📜 Declared by directors

- Recorded in corporate records

- Supported by retained earnings

Proper declaration usually requires:

- A board resolution

- Documentation in the minute book

- Confirmation that share structure allows payment

Without documentation, the dividend may not legally exist.

📁 Corporate Minute Book & Legal Documentation

In many cases, you will need to:

- Prepare a dividend resolution

- Coordinate with the corporate lawyer

- Ensure share classes permit dividend distribution

- Record the declaration date

If multiple share classes exist, dividends must follow the share structure rules.

Administrative discipline protects the client.

🚨 The TOSI Rules (Tax on Split Income)

Dividend planning changed significantly due to TOSI rules.

Under TOSI:

- Certain dividends paid to family members

- May be taxed at the highest marginal tax rate

This restricts “income sprinkling.”

TOSI commonly affects:

- Spouses

- Adult children

- Minor children

- Related individuals

Before recommending dividends to family members, you must determine whether:

- An exception applies

- The business qualifies as excluded

- The shareholder meets active involvement tests

Never assume dividend splitting is permitted.

👨👩👧 When TOSI May Not Apply

TOSI may not apply if:

- The individual works actively in the business

- Ownership and age tests are satisfied

- The corporation meets excluded business criteria

Each case must be reviewed carefully.

This is now a core compliance step in dividend planning.

🧾 Filing Requirements for Dividends

When dividends are paid, you must:

- Prepare T5 slips

- File a T5 summary

- Report dividend income on the shareholder’s T1 return

T5 slips are generally due by the end of February following the calendar year.

Late filing penalties apply.

📋 Administrative Checklist Before Paying Dividends

Before dividends are issued:

- ✅ Confirm retained earnings are sufficient

- ✅ Verify share structure

- ✅ Prepare director resolution

- ✅ Record declaration date

- ✅ Record dividend payable in accounting records

- ✅ Issue payment

- ✅ Prepare and file T5 slips

This checklist should become routine in your practice.

🧠 Why Proper Administration Matters

Improper dividend handling can lead to:

- Reclassification issues

- Shareholder loan problems

- TOSI reassessments

- CRA scrutiny

- Legal documentation deficiencies

Clean administration reduces audit risk.

🏆 Key Takeaway

Dividends are not simpler than salary — they are different.

They require:

✔ Proper legal declaration

✔ Careful TOSI review

✔ Accurate documentation

✔ Timely T5 filing

✔ Clear communication with shareholders

Understanding dividend administration is essential for any tax preparer working with corporate owner-managers.

🏛 Review the Classes of Shares to Ensure Dividends Can Be Paid

Before declaring or planning any dividend, you must confirm one critical thing:

❓ Do the shareholder’s shares actually allow dividends to be paid?

This is the first administrative step in dividend planning — and it is often overlooked by beginners.

Dividends are not simply “money taken out of the company.” They must be legally permitted under the corporation’s share structure.

📘 Why This Step Comes First

Even if:

- The corporation has profit

- The owner wants money

- The tax plan recommends dividends

You cannot proceed unless the share class allows it.

Ignoring this step can lead to:

- ❌ Invalid dividend declarations

- ❌ Paying the wrong shareholder

- ❌ Legal non-compliance

- ❌ CRA scrutiny

- ❌ Professional liability

📂 Step 1: Review the Minute Book (Always)

Never rely on what the client tells you.

Many clients say:

“We both own the company.”

That is not enough.

You must physically review:

- Articles of incorporation

- Share class descriptions

- Share register

- Shareholder agreements

- Any amendments to the articles

The minute book tells you:

- Who owns what class of shares

- What rights those shares carry

- Whether dividends are restricted

This step protects you.

🧾 Understanding Share Classes (Beginner Friendly)

Corporations can issue different types of shares:

- Common shares

- Preferred shares

- Special shares (Class A, Class B, etc.)

Each class can have:

- Voting rights

- Dividend rights

- Restrictions

- Priority rules

The dividend rights are what matter for compensation planning.

🟢 Scenario 1: Single Class of Common Shares

If:

- There is only one shareholder

- Only common shares exist

- No restrictions are listed

Dividends are usually straightforward.

This is the simplest structure.

🔵 Scenario 2: Multiple Classes for Income Splitting

Often corporations are structured like this:

- Spouse 1 owns common shares

- Spouse 2 owns special shares

This structure allows flexibility in dividend allocation.

However — you must confirm that:

- The special shares allow unlimited dividends

- There are no percentage caps

- There are no priority restrictions

⚠️ Common Restriction #1: Dividend Caps

Some incorporations (especially online templates) include clauses such as:

Dividends limited to a fixed percentage (e.g., 8%) of stated value.

Example:

If shares have $100 stated value and an 8% cap:

Maximum dividend = $8 per share

You cannot legally declare a large discretionary dividend.

If you attempt to, the dividend may not be valid.

⚠️ Common Restriction #2: Preferred Shares Paid First

Preferred shares often contain priority clauses like:

Preferred shareholders must receive dividends before common shareholders.

If:

- One spouse owns preferred shares

- The other owns common shares

You may be legally required to pay the preferred shareholder first.

If ignored, this can:

- Redirect income unintentionally

- Cause family disputes

- Trigger tax complications

Always check priority rules.

🚨 Why This Matters Even More Today

Dividend payments are increasingly scrutinized, especially where family members are involved.

With modern income-splitting restrictions and compliance reviews, tax authorities may examine:

- Share structures

- Dividend patterns

- Ownership documentation

If your dividend plan does not align with share rights, problems can arise quickly.

📞 When Share Structure Prevents Your Plan

If you discover that:

- Dividends are capped

- Priority rules prevent flexibility

- Share classes are poorly structured

Do not try to “work around” the issue.

Recommend consultation with:

- A corporate lawyer

- A corporate tax lawyer

They may suggest:

- Share reorganization

- Amending articles

- Creating new share classes

These changes must be done properly to avoid tax consequences.

📋 Professional Best-Practice Checklist

Before declaring dividends, confirm:

✔ Corporation has sufficient retained earnings

✔ Shareholder owns dividend-eligible shares

✔ No dividend caps exist

✔ No priority rules conflict

✔ Share register matches intended payment

✔ Documentation will be prepared

Document your review in your working papers.

🏆 Final Takeaway

Dividend planning starts with structure.

Before calculating tax savings or preparing T5 slips, you must first confirm:

📖 The share class allows dividends to be paid — in the amount and manner you intend.

If you master this step, you prevent administrative errors and protect both your client and your professional reputation.

📊 Calculations May Be Necessary to Determine Per Share Dividend Amounts

When declaring dividends in a corporation, you cannot simply decide how much each shareholder will receive.

Dividends must always be calculated:

💡 On a per-share basis

This is not optional. It is how dividends are legally declared and recorded in corporate minute books.

If you skip this step, your documentation will be incorrect.

🧠 Why Dividends Must Be Calculated Per Share

Dividends are paid:

Per share — not per person.

The total dividend declared must be divided among the issued and outstanding shares of a specific class.

That per-share amount determines:

- How much each shareholder receives

- What gets recorded in the minute book

- What appears on each T5 slip

- Whether the allocation is legally correct

This is basic corporate law administration.

🔹 Example 1: Single Class of Common Shares

Assume:

- $100,000 dividend declared

- 100 common shares outstanding

- Two shareholders:

- Jason owns 67 shares

- Richard owns 33 shares

Step 1: Calculate Dividend Per Share

Total dividend ÷ Total shares

$100,000 ÷ 100 shares = $1,000 per share

Step 2: Allocate to Shareholders

Jason:

67 shares × $1,000 = $67,000

Richard:

33 shares × $1,000 = $33,000

There is no flexibility here.

Common shares must share equally per share.

You cannot choose a different split.

🔹 Example 2: Two Different Classes of Shares

Now assume:

- $100,000 total dividends declared

- Two classes:

- Common shares (Jason owns 100)

- Special shares (Richard owns 100)

The board declares:

- $67,000 dividend on common shares

- $33,000 dividend on special shares

Step 1: Calculate Per Share for Each Class

Common shares:

$67,000 ÷ 100 shares = $670 per share

Special shares:

$33,000 ÷ 100 shares = $330 per share

Important Rule

Each share class has its own per-share calculation.

You do not mix share classes.

If you mistakenly apply:

$1,000 per share to both classes

You would incorrectly allocate $100,000 to each class — doubling the intended dividend.

This is why careful calculations matter.

🔹 Example 3: Clearing a Shareholder Loan (Odd Amounts)

Sometimes dividends are declared to clear a shareholder loan balance.

Assume:

- Shareholder loan balance = $41,282.50

- Shareholder owns 37 shares of Class C

Step 1: Calculate Per Share

$41,282.50 ÷ 37 shares = $1,115.7432 per share

Yes — fractional cents are acceptable.

Dividends can include decimals.

You must calculate precisely to match the declared total.

If you round improperly, the total dividend will not reconcile.

📂 Why This Matters for Documentation

Corporate resolutions typically state:

“A dividend of $X per share is declared on Class ___ shares.”

Not:

“We are paying $100,000 total.”

The per-share amount is what makes the declaration legally valid.

It is also what lawyers record in the minute book.

📋 Administrative Checklist for Per-Share Calculations

Before preparing dividend documentation:

✔ Confirm number of issued and outstanding shares

✔ Confirm share class being paid

✔ Confirm total dividend declared

✔ Divide total by shares in that class

✔ Calculate exact per-share amount

✔ Multiply per-share amount by shares held by each shareholder

✔ Confirm totals reconcile exactly

⚠️ Common Mistakes Beginners Make

❌ Dividing by total shares across all classes

❌ Forgetting different classes require separate calculations

❌ Rounding incorrectly

❌ Allocating dividends based on percentages without calculating per-share

❌ Declaring total amount without computing per-share figure

🏛 Why Accuracy Is Important

Dividend records may be reviewed by:

- Corporate lawyers

- Accountants

- Tax authorities such as the Canada Revenue Agency

If per-share amounts do not reconcile:

- Minute book entries may be invalid

- T5 slips may be incorrect

- Dividend allocations could be challenged

🏆 Final Takeaway

Dividends are always declared:

📌 On a per-share basis

📌 By share class

📌 Based on issued and outstanding shares

Whenever you declare a dividend:

- Identify the class

- Count the shares

- Divide total dividend by shares

- Allocate accurately

Master this step and your dividend administration will be precise, professional, and legally sound.

⚖️ Consider the New Rules for Paying Dividends – The Over-Arching Principle (TOSI Explained)

Dividend planning in Canada changed dramatically after the introduction of the Tax on Split Income (TOSI) rules.

If you are becoming a tax preparer, this is one of the most important mindset shifts you must understand.

Before TOSI, many corporations used dividend sprinkling (also called income splitting) to reduce overall family tax.

Today, the rules are much stricter.

This section will give you the big-picture principle you must always keep in mind when advising on dividends.

📜 What Are the TOSI Rules?

The TOSI rules were introduced through federal legislation (Bill C-74) and apply to certain types of income, including dividends received from private corporations.

They are enforced by the Canada Revenue Agency.

If TOSI applies:

💥 The dividend is taxed at the highest marginal personal tax rate.

No dividend tax credit benefit.

No low-income family advantage.

No income-splitting benefit.

In simple terms:

If you try to split income improperly, the tax savings disappear.

🎯 The Over-Arching Principle (The 300,000-Foot View)

Forget the complex rules for a moment.

Here is the guiding principle:

If the only reason a person owns shares is to save tax — TOSI will likely apply.

Ask yourself this:

- Did this shareholder invest capital?

- Did they contribute labour?

- Did they take financial risk?

- Did they guarantee loans?

- Are they actively involved in the business?

If the answer is “no” to all of the above…

And they are receiving dividends…

That is a red flag.

🧠 Think Like an Independent Third Party

A helpful way to analyze dividend situations is to step back and ask:

If this person was NOT related to the owner, would the company give them shares and pay them dividends?

If the answer is:

“No, that would make no business sense.”

Then you may be dealing with TOSI exposure.

Corporations do not normally give equity and dividends to people who:

- Contributed no money

- Provided no work

- Took no risk

- Provided no guarantees

If the only explanation is tax savings, that’s the danger zone.

👨👩👧 Why Family Dividends Are Under Scrutiny

Most TOSI situations involve:

- Spouses

- Adult children

- Minor children

- Other related individuals

Before TOSI, it was common to:

- Issue shares to family members

- Pay dividends to lower-income relatives

- Reduce overall family tax burden

Now, those arrangements are carefully examined.

If the dividend recipient is not genuinely contributing to the business, the income may be reclassified under TOSI.

🚨 What Happens If TOSI Applies?

If caught by TOSI:

- Dividend is taxed at top personal rate

- No benefit from lower marginal brackets

- No effective income splitting

- Potential reassessment and interest

This can significantly increase the tax bill.

📌 Important Distinction: Salary vs Dividend

TOSI mainly targets dividend income and certain other types of income.

Salary paid for actual work is generally not affected in the same way, provided it is reasonable.

That is why, in some cases, paying a reasonable salary may be safer than paying dividends.

🔍 The Logical Test You Should Always Apply

Before advising on dividend payments, ask:

- Why does this shareholder own shares?

- What value did they provide to the corporation?

- Would an unrelated third party in the same position receive dividends?

- Is this arrangement commercially reasonable?

- Is the primary motivation tax savings?

If the arrangement exists solely for tax reduction, you are likely on what some practitioners informally call the “TOSI train.”

🏛 Legislative Background (For Context)

The TOSI regime was expanded significantly in 2018 to address income sprinkling in private corporations.

It reflects a policy decision that:

Income should be taxed in the hands of those who genuinely earned or invested for it.

As a tax preparer, you are not just calculating numbers — you are evaluating substance.

📋 Practical Mindset for Beginners

When reviewing a client file:

✔ Identify all shareholders

✔ Determine relationships between them

✔ Understand their involvement in the business

✔ Review capital contributions

✔ Review loan guarantees

✔ Review historical dividend patterns

Then apply the overarching principle:

If this looks like pure tax splitting with no real business purpose, assume TOSI risk until proven otherwise.

🏆 Final Takeaway

The TOSI rules changed dividend planning completely.

You must move from:

“Can we split income to save tax?”

To:

“Does this shareholder genuinely deserve dividends based on capital, risk, or contribution?”

If not, the dividend may be taxed at the highest rate.

Master this overarching principle, and you will be far better prepared to navigate the detailed TOSI rules that follow.

🚂 TOSI – Weaving Through the Complexities of the New Rules

The Tax on Split Income (TOSI) rules have fundamentally changed how dividends can be paid within family-owned corporations.

If you are training to become a tax preparer, you must understand this:

⚠️ Dividend sprinkling is no longer simple — and often no longer effective.

TOSI adds layers of complexity that directly impact owner-manager compensation planning.

Let’s break this down in a structured, beginner-friendly way.

🧾 First: TOSI Is Not Completely New

TOSI has existed in some form since 1999.

You may have heard of the “kiddie tax.”

Under the original rules:

- Dividends paid to minor children (under 18)

- Were taxed at the highest marginal tax rate

This rule still exists.

For example:

If a 17-year-old receives a $100,000 dividend:

That income is taxed at the highest personal rate in their province.

There is no income-splitting advantage.

🔍 What Changed With the New TOSI Rules?

The major expansion of TOSI occurred in 2018.

The goal was to eliminate most forms of:

- Dividend sprinkling

- Family income splitting

- Passive shareholder tax planning

The rules are administered by the Canada Revenue Agency.

They now apply to:

- Certain adults aged 18–24

- Adults aged 25+

- Indirect ownership structures

- Trust structures

- Holding companies

- Related business income

This is where complexity increases.

📌 Who Does TOSI Potentially Apply To?

TOSI applies to income received:

By a specified individual

From a related business

In simple English:

If someone receives dividends from a business controlled by a related person (usually family), TOSI may apply.

This includes situations involving:

- Parents and children

- Spouses

- Corporations owned by family members

- Holding companies

- Trust beneficiaries

It is intentionally broad.

💥 What Happens If TOSI Applies?

If income is caught under TOSI:

- It is taxed at the highest marginal rate

- Most personal tax credits cannot be used

- Dividend tax credit benefits are effectively neutralized

In practice:

The tax savings disappear.

👶 Age Categories Matter

One reason TOSI is complex is because different rules apply depending on age:

- Under 18 → Automatic highest rate (kiddie tax)

- Age 18–24 → Additional restrictive tests

- Age 25+ → Different exclusion tests

Each age bracket has different qualification criteria.

This is why reviewing shareholder age is now a standard compliance step.

🧠 The Core Practical Rule

Always ask:

Is this shareholder genuinely involved in the business?

If they are not:

- No capital invested

- No labour provided

- No risk taken

- No guarantees signed

Then dividends paid to them are high risk for TOSI.

If the only reason they own shares is to reduce tax:

That is exactly what the legislation targets.

⚙️ Why TOSI Is So Complex

The legislation uses broad language like:

“Specified individuals receiving income from a related business directly or indirectly.”

That wording captures:

- Holding companies

- Multi-tier corporate structures

- Trust ownership arrangements

- Indirect shareholdings

It is intentionally comprehensive.

That is why TOSI analysis often feels overwhelming.

📉 Practical Reality for Owner-Managers

Because of TOSI:

Many corporations now avoid paying dividends to:

- University-age children

- Non-active adult children

- Passive spouses

Instead, they may:

- Pay reasonable salaries

- Or restrict dividends to active shareholders

This shifts planning away from dividend sprinkling and back toward employment-based compensation.

⚠️ Why We Call It the “TOSI Train”

Once income falls under TOSI:

It is difficult to escape the highest-rate taxation.

The goal becomes:

Identifying exclusions before paying dividends.

If you cannot confidently qualify for an exclusion, the conservative approach may be to avoid dividends altogether.

📋 Beginner Compliance Checklist

When reviewing dividends:

✔ Identify all shareholders

✔ Confirm ages

✔ Confirm involvement in business

✔ Confirm capital contribution

✔ Review related ownership structures

✔ Review holding companies or trusts

✔ Assess whether an exclusion applies

If no clear exclusion applies:

Assume TOSI risk.

🏛 The Current Landscape

The expanded TOSI rules are relatively new in legislative history.

Administrative interpretation continues to evolve.

The Canada Revenue Agency may refine enforcement patterns over time.

For now, conservative planning is common.

🏆 Final Takeaway

TOSI changed dividend planning permanently.

You must shift from:

“How can we split income?”

To:

“Does this shareholder legitimately qualify to receive dividends?”

If not, the income will likely be taxed at the highest personal rate.

Understanding this framework is essential before diving into the specific exclusions and detailed tests that follow.

🚂 Getting Off the TOSI Train and Meeting an Exception

When analyzing dividends under the Tax on Split Income (TOSI) rules, you must start with the correct mindset:

🔴 Assume TOSI applies first.

🟢 Then look for an exception.

This is the safest and most professional way to approach dividend planning for corporate owner-managers.

Think of TOSI like a train 🚂.

By default, every dividend recipient is on the train.

Your job as a tax preparer is to determine whether they can legally step off.

🧠 The Default Position: Everyone Is On the TOSI Train

Before you begin analyzing exclusions, understand this:

Under the expanded TOSI rules administered by the Canada Revenue Agency, dividends paid from a related business are generally assumed to be subject to TOSI unless an exception applies.

That means:

- Owner-managers

- Spouses

- Adult children

- Trust beneficiaries

- Holding company shareholders

All start on the train.

The burden is on you to determine whether they qualify to get off.

🚪 The “Doors” – Each Exception Is a Way Off the Train

Imagine each TOSI exception as a door on the train.

If the dividend recipient qualifies under any one exception, they step off.

Once they are off:

✅ TOSI no longer applies to that income.

❌ You do not need to test the other exceptions.

This is extremely important.

You do not need to satisfy all exceptions.

You only need to satisfy one.

🔍 How the Analysis Works in Practice

When reviewing a dividend payment, you work through the exclusions systematically.

For example:

- Is this an excluded business?

- Does the shareholder own excluded shares?

- Is the amount considered an excluded amount?

- Does a safe harbour test apply?

- Is the shareholder actively engaged?

You test each category one by one.

If one applies, you stop.

The person steps off the TOSI train.

📦 Key Concept: You Don’t Re-Board the Train

Once a shareholder qualifies under one exception:

They are not required to pass other tests.

For example:

If someone qualifies under the excluded shares exception:

You do not need to worry whether they qualify under the excluded business test.

They are already off the train.

This prevents unnecessary over-analysis.

⚖️ Example Scenario

Assume:

- A 30-year-old shareholder receives dividends.

- You begin reviewing TOSI.

You test:

- Excluded business? ❌ No.

- Excluded shares? ✅ Yes.

At that point, you stop.

TOSI does not apply.

You do not continue testing other exceptions.

📋 Why This Structured Approach Is Critical

The TOSI legislation is complex and layered.

Without structure, it can feel overwhelming.

By using the “train and doors” approach, you:

✔ Start from a conservative position

✔ Work methodically through exceptions

✔ Avoid missing an applicable exclusion

✔ Avoid unnecessary panic

✔ Apply consistent analysis across clients

This makes your workflow repeatable and defensible.

⚠️ Common Mistake Beginners Make

Many new tax preparers:

- Read one exception.

- Realize their client does not meet it.

- Assume TOSI automatically applies.

This is incorrect.

Failure to meet one exception does not mean failure overall.

You must test each possible exit.

🧾 Why This Matters for Owner-Managers

Family-owned corporations often involve:

- Multiple share classes

- Spouses

- Adult children

- Holding corporations

- Trust structures

Without a systematic process, it is easy to misapply TOSI.

The “TOSI Train” framework helps simplify decision-making in complex files.

📌 Administrative Best Practice

When reviewing dividend payments:

- Assume TOSI applies.

- Document each exception reviewed.

- Note which exception applies (if any).

- Stop once one exception is satisfied.

- Keep documentation in your working papers.

This protects both you and your client.

🏁 Final Takeaway

TOSI analysis is not about proving someone qualifies under every rule.

It is about finding one valid exception.

Remember:

🚂 Everyone starts on the train.

🚪 Each exception is a door.

✅ One open door is enough.

Once off the train, the dividend is no longer subject to TOSI.

This structured mindset will make navigating the complex TOSI rules far more manageable as you move deeper into each individual exception.

🚪 What Are the Exceptions and Excluded Amounts to TOSI?

Once you understand that everyone starts on the TOSI train, the next logical question is:

👉 How does someone legally get off?

Under the expanded Tax on Split Income (TOSI) regime administered by the Canada Revenue Agency, certain “excluded amounts” are carved out.

If a dividend qualifies as an excluded amount, it is not subject to TOSI and will be taxed normally.

For small business owner-managers, there are three primary exclusions you must understand:

- 🧠 Reasonable Return (Logic Test)

- 👷 Excluded Business (Active Involvement Test)

- 🏢 Excluded Shares (Good Shares Test)

While legislation includes more technical categories, these three are the most relevant for corporate owner-manager planning.

Let’s break them down clearly.

🧠 1️⃣ The Reasonable Return Test (The Logic Test)

This is often called the “reasonable return” exception.

At its core, it asks:

Is the dividend reasonable based on the shareholder’s contributions?

Contributions may include:

- 💰 Capital invested

- 🧾 Assets contributed

- 💼 Work performed

- 📊 Risk assumed

- 📑 Guarantees provided

If the dividend reflects a reasonable return relative to those contributions, it may qualify as an excluded amount.

📌 Practical Example

Imagine:

- A shareholder invested $100,000 into a corporation.

- They receive a $5,000 dividend.

That is roughly a 5% return.

From a commercial perspective, that is reasonable.

Now compare that to:

- A shareholder who invested $1.

- They receive a $30,000 dividend.

That is not commercially reasonable in an arm’s length scenario.

The government asks:

Would an unrelated third party receive this return?

If the answer is no, TOSI risk increases.

⚠ Important Clarification

This test becomes stricter for individuals aged 18–24.

The legislation applies more restrictive standards to younger shareholders.

This means the “reasonable return” test is more limited for that age group.

👷 2️⃣ Excluded Business (Active Involvement Test)

This is the most important exclusion for small owner-managed businesses.

It is commonly referred to as the active involvement test.

To qualify:

The individual must be actively engaged in the business on a regular, continuous, and substantial basis.

This is often interpreted as meeting a bright-line threshold of 20 hours per week during the year (or historically meeting that threshold in prior years).

🏗 Example – Clearly Active

- George owns 100% of George’s Electrical Services Inc.

- He works full-time running jobs, managing staff, and performing electrical work.

George clearly qualifies under the excluded business rule.

Dividends paid to him are not subject to TOSI.

👩💼 Example – Spouse Involvement

- George’s spouse works 25 hours per week doing bookkeeping and administration.

If documentation supports regular and continuous involvement, she may qualify under the excluded business exception.

This is where documentation matters:

✔ Timesheets

✔ Payroll records

✔ Role descriptions

✔ Evidence of duties

🚨 Warning

If a shareholder:

- Owns shares

- Does not work in the business

- Does not contribute capital meaningfully

- Does not assume risk

They likely do not meet this exclusion.

🏢 3️⃣ Excluded Shares (The “Good Shares” Exclusion)

This is the most technical and restrictive exclusion.

To qualify, several conditions must be met, including:

- The shareholder owns at least 10% of votes and value.

- The corporation earns less than 90% of its income from services.

- The corporation is not a professional corporation.

- The income is not derived from a related business providing services.

⚖ Why This Is Complicated

This exclusion:

❌ Generally does not apply to professional corporations

- Doctors

- Dentists

- Lawyers

- Accountants

❌ Often does not apply to service-based businesses

The government intentionally limited this exclusion for service-type corporations.

It is more commonly available for:

- Manufacturing companies

- Product-based businesses

- Non-professional operating companies

📊 Quick Comparison Table

| Exclusion Type | Key Requirement | Most Relevant For | Complexity Level |

|---|---|---|---|

| 🧠 Reasonable Return | Dividend must reflect fair commercial return | Shareholders who contributed capital | Moderate |

| 👷 Excluded Business | Active, regular, substantial involvement | Owner-managers & working spouses | Most Common |

| 🏢 Excluded Shares | 10% vote & value + non-service income | Non-service businesses | High |

🎯 Which Exclusion Matters Most for Small Businesses?

For typical owner-managed corporations:

👉 The Excluded Business (Active Involvement) test is the most practical and commonly used.

The Reasonable Return test may apply in capital-heavy structures.

The Excluded Shares test is less common in service-based corporations.

📌 Practical Workflow for Tax Preparers

When reviewing dividends:

- Start with the assumption that TOSI applies.

- Test for Excluded Business first.

- If not met, test Reasonable Return.

- If applicable, analyze Excluded Shares.

- Document your reasoning.

If any one exclusion applies:

✅ TOSI does not apply.

🚪 The shareholder steps off the train.

⚠ The Overarching Reality

TOSI was designed to eliminate pure dividend sprinkling.

If dividends are paid to:

- Non-active family members

- Individuals who contributed little capital

- Passive shareholders

They are high-risk for TOSI.

The legislation forces business owners to justify dividend payments with economic substance.

🏁 Final Takeaway

For small business owner-managers, TOSI analysis revolves around three pillars:

🧠 Is the return reasonable?

👷 Is the shareholder actively involved?

🏢 Do the shares qualify as excluded shares?

Mastering these three concepts gives you a strong foundation for navigating dividend planning under modern TOSI rules.

As a developing tax preparer, this framework will allow you to approach dividend files with structure, confidence, and compliance awareness.

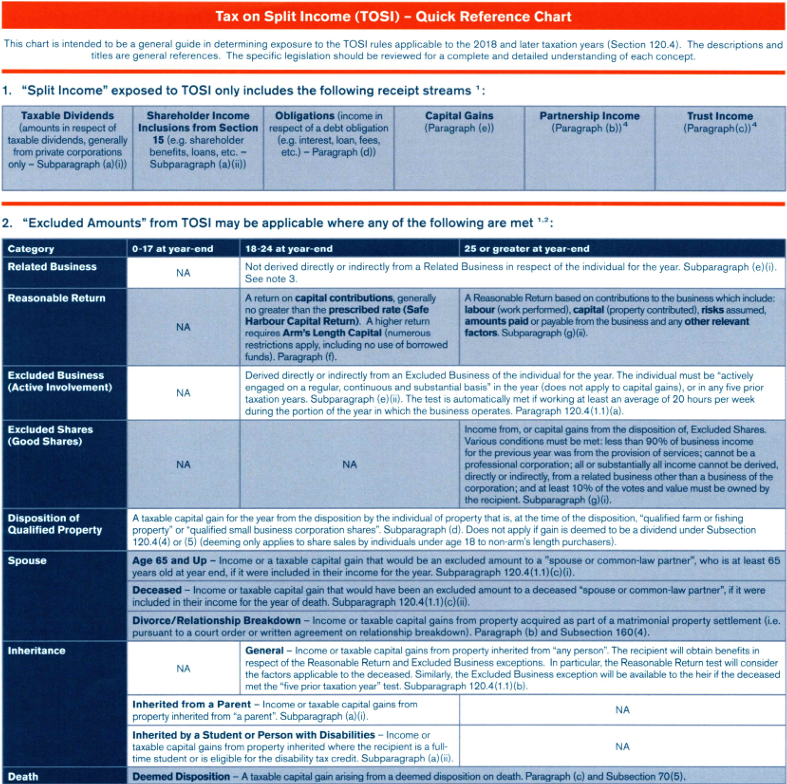

📊 Quick Reference Chart & CRA Resources to Help You Navigate the Complex TOSI Rules

The Tax on Split Income (TOSI) rules are among the most complex provisions in Canadian personal tax planning.

Even experienced practitioners attend multi-hour seminars just to stay current.

As a beginner tax preparer, your goal is not to memorize every paragraph of legislation — it is to develop:

✔ A structured approach

✔ A decision-making framework

✔ A reliable reference tool

✔ Awareness of where to research further

This is where a quick reference chart and official guidance from the Canada Revenue Agency become essential.

🧾 Step 1: What Income Is Even Subject to TOSI?

Before you look at exceptions, you must confirm whether the income is the type captured by TOSI.

The quick reference chart breaks income into specific categories, including:

- 💰 Taxable dividends (private corporations)

- 📌 Shareholder benefits (Section 15 inclusions)

- 📜 Certain shareholder income inclusions

- 💳 Obligations (interest, loans, etc.)

- 📈 Capital gains (in certain cases)

- 🤝 Partnership income

- 🏦 Trust income

While legislation lists categories individually, practically speaking:

If a shareholder receives income from a related business, assume TOSI risk exists.

Once income is identified as potentially caught, you are “on the TOSI train.”

Now the analysis begins.

🚪 Step 2: Use the Chart to Identify Excluded Amounts (Your Exit Doors)

The reference chart organizes all excluded amounts into clear categories.

Each row represents a potential exit from TOSI.

If one applies, the dividend is taxed normally.

You do NOT need to qualify under every exception.

You only need one.

🧠 The Most Relevant Exclusions for Small Business Owner-Managers

While the chart lists many technical exclusions, for small owner-managed corporations, focus primarily on:

👷 Excluded Business (Active Involvement)

The individual must be actively engaged in the business on a regular, continuous, and substantial basis.

This is the most common and practical exclusion.

🧠 Reasonable Return

The dividend must reflect a reasonable return based on:

- Capital contributed

- Work performed

- Risks assumed

- Guarantees provided

If it resembles what an arm’s length investor would receive, it may qualify.

🏢 Excluded Shares

This requires meeting multiple technical tests including:

- 10% ownership of votes and value

- Less than 90% service income

- Not a professional corporation

- Limited related service income

This exclusion is detailed and often does NOT apply to service-based corporations (e.g., doctors, lawyers, accountants).

📌 Other Exclusions You Must Be Aware Of

Even if they are less common in small business files, you must understand they exist:

🏞 Disposition of Qualified Property

Includes:

- Qualified small business corporation shares

- Qualified farm or fishing property

These may be excluded from TOSI in capital gain situations.

👵 Age 65+ Spousal Exception

If a spouse is age 65 or older, dividends may qualify for exclusion similar to pension income splitting concepts.

This prevents unfair taxation on long-built family capital.

⚖ Divorce or Relationship Breakdown

Property received under court order or written separation agreements may qualify for exclusion.

⚰ Death & Deemed Disposition

Capital gains triggered on death are not meant to be subject to punitive TOSI treatment.

🎁 Inheritance

If adult children inherit shares, certain exclusions may apply.

The chart helps identify whether:

- The inherited amount qualifies

- Active involvement tests can transfer

- Reasonable return logic can apply

📊 Why the Chart Is So Powerful

Instead of flipping through legislative paragraphs, the chart gives you:

- Income types

- Age categories (0–17, 18–24, 25+)

- Applicable exclusions

- Legislative references

- Special notes

It allows you to visually:

- Identify the income

- Identify the age bracket

- Test the exclusions

- Confirm documentation requirements

🗂 Age Categories Matter — Always Check This First

The chart separates rules by age:

| Age Group | TOSI Strictness |

|---|---|

| 0–17 | Automatic highest tax (kiddie tax) |

| 18–24 | More restrictive tests |

| 25+ | Broader exclusions available |

This is critical.

Many beginners forget that age directly affects eligibility for exclusions.

📚 Why You Still Need to Review CRA Guidance

The chart is a summary tool.

But you must also:

- Review technical interpretations

- Monitor CRA updates

- Stay current with administrative guidance

The Canada Revenue Agency regularly publishes:

- Folios

- Technical interpretations

- Income Tax Technical News

- Updated administrative positions

TOSI is still evolving.

Enforcement patterns are developing.

⚠️ Important Professional Reality

Entire professional seminars are devoted solely to TOSI.

This means:

- You will not master it in one lesson.

- You must develop comfort with research.

- You must document your reasoning carefully.

If unsure, conservative planning is often safer.

🧩 Practical Workflow Using the Chart

When reviewing a dividend file:

1️⃣ Identify income type

2️⃣ Confirm shareholder age

3️⃣ Assume TOSI applies

4️⃣ Review exclusions row-by-row

5️⃣ Stop once one exclusion applies

6️⃣ Document the analysis

This structured process makes complex legislation manageable.

🏁 Final Takeaway

The quick reference chart is not a shortcut.

It is a navigation map.

TOSI is complex because it tries to prevent artificial income splitting while allowing legitimate business participation.

As a developing tax preparer, your responsibility is:

✔ Know what income is caught

✔ Understand the main exclusions

✔ Use structured tools

✔ Stay current with CRA guidance

✔ Document every decision

Mastering this framework will give you confidence when analyzing dividend compensation under modern TOSI rules.

👷 Excluded Business Test for Active Involvement in the Business

When dealing with dividends under the Tax on Split Income (TOSI) regime, this is the exclusion you will rely on the most as a tax preparer working with corporate owner-managers.

For small family-owned corporations, the Excluded Business Test (Active Involvement Test) is often the strongest and most practical way to avoid TOSI applying to dividend income.

If this test is met:

✅ The dividend becomes an “excluded amount”

🚪 The shareholder steps off the TOSI train

💰 Dividends are taxed normally — not at the highest marginal rate

This section will give you a complete, practical understanding of how this exclusion works and how to apply it in real client files.

📌 Why the Excluded Business Rule Exists

The government and the Canada Revenue Agency recognize a simple reality:

Family members often genuinely work in family businesses.

If someone:

- Actively works in the corporation

- Contributes meaningful labour

- Helps generate income

It would be unfair to tax their dividends at the punitive TOSI rate.

So the law allows an exclusion — but only if strict conditions are satisfied.

🔎 Core Eligibility Requirements

To qualify under the Excluded Business Test, the following conditions must be met:

1️⃣ The individual must be 18 years of age or older

2️⃣ The individual must be actively engaged in the business

3️⃣ The engagement must be regular, continuous, and substantial

Each of these words matters.

🚫 Age Requirement – No Minors Allowed

The exclusion does not apply to anyone under 18.

If a minor receives dividends:

❌ The kiddie tax rules apply

❌ Automatic taxation at the highest marginal rate

There is no workaround through the excluded business test for minors.

🔥 The Bright-Line Rule: 20 Hours Per Week

To simplify administration, the CRA introduced a bright-line threshold.

If the individual works:

📌 An average of at least 20 hours per week

📌 During the portion of the year the business operates

Then the “regular, continuous and substantial” test is automatically considered met.

This is extremely important.

It gives you an objective measurement.

🏗 What Does “During the Portion of the Year the Business Operates” Mean?

Some businesses are seasonal.

Examples include:

- Landscaping companies

- Snow removal businesses

- Seasonal tourism operations

- Agricultural operations

If a business operates only four months per year:

The 20-hour average applies only during those operating months.

You do not need 20 hours per week for the entire 12 months.

🧠 Real-Life Application Examples

✅ Example 1 – Full-Time Owner-Manager

- Works 40–60 hours per week

- Actively runs operations

- Makes business decisions

Clearly qualifies.

No TOSI concern under this exclusion.

✅ Example 2 – Spouse Working 25 Hours Per Week

- Manages bookkeeping

- Handles payroll

- Coordinates scheduling

- Manages accounts receivable

If averaging 20+ hours per week:

Dividends can qualify as excluded amounts.

❌ Example 3 – Adult Child Working 8–10 Hours Per Week

- Helps occasionally

- No structured role

- No documentation

Likely fails the bright-line test.

Dividends would likely be subject to TOSI.

📅 The Five-Year Historical Lookback Rule

This is one of the most powerful aspects of this exclusion.

Even if the individual does NOT meet the 20-hour threshold in the current year, the exclusion can still apply if:

✔ The individual worked an average of 20 hours per week

✔ In any five prior taxation years

Important clarifications:

- The five years do NOT need to be consecutive.

- They can be any five prior years.

- Once satisfied, the exclusion continues to apply going forward.

🧩 Example of the Five-Year Rule in Action

Adult child:

- Worked 20–25 hours per week during university summers

- Met threshold for five separate years

- Now has a full-time job elsewhere

Even though they no longer work in the business:

They may still qualify under the excluded business test.

This allows long-term dividend flexibility.

📂 Documentation: Your Protection in Case of CRA Review

Meeting the rule is one thing.

Proving it is another.

The CRA evaluates this on a factual, case-by-case basis.

You must maintain documentation.

📋 Recommended Documentation Checklist

✔ Timesheets

✔ Payroll records

✔ T4 slips

✔ Employment agreements

✔ Job descriptions

✔ Email communications

✔ Proof of responsibilities

✔ Historical payroll summaries

✔ Board resolutions referencing roles

If audited, documentation will determine success or failure.

⚠ Common Practical Challenge: Historical Proof

The five-year rule creates a real issue:

Most small businesses did not historically track detailed hours for family members.

If you plan to rely on past years:

You may need to reconstruct evidence using:

- Payroll records

- Historical T4 amounts

- Banking records

- Internal correspondence

- Sworn statements

The CRA has indicated flexibility, but proof must still be reasonable and credible.

📊 What Counts as “Substantial” Work?

The 20-hour test helps — but the work must also be meaningful.

Strong Examples of Substantial Work:

- Operations management

- Technical services

- Client management

- Financial oversight

- Administrative coordination

- Production supervision

Risky or Weak Examples:

- Occasional cleaning only

- Minimal social media posting

- Token symbolic duties

- Inflated reporting of hours

Substance matters.

The more essential the work is to business operations, the stronger your position.

📌 Quick Reference Summary Table

| Requirement | Must Be Met? | Key Notes |

|---|---|---|

| Age 18+ | Yes | No minors qualify |

| 20 hours/week average | Yes (bright-line) | During operating period |

| OR 5 prior qualifying years | Yes | Not consecutive |

| Regular, continuous, substantial | Yes | Evaluated factually |

| Documentation | Critical | Protects against reassessment |

🎯 Why This Is the Most Important TOSI Exclusion for Owner-Managers

For small corporations:

- Family members often legitimately work in the business

- Spouses commonly manage administration

- Adult children may help long-term

This exclusion preserves dividend flexibility for genuine contributors.

Without it, many family businesses would be forced to abandon dividend planning entirely.

🏁 Final Takeaway for New Tax Preparers

When reviewing dividend files under TOSI:

1️⃣ Confirm the individual is 18 or older

2️⃣ Verify 20 hours per week average (or 5 prior qualifying years)

3️⃣ Ensure work is meaningful and substantial

4️⃣ Gather and preserve documentation

5️⃣ Record your analysis in working papers

If those elements are satisfied:

🚪 The shareholder steps off the TOSI train

💰 Dividends are not subject to the highest marginal tax rate

Master this exclusion first.

It will be the cornerstone of your dividend planning strategy under modern TOSI rules.

💰 Reasonable Return Test for Reasonable Return on Capital Put Into the Business

The Reasonable Return Test is one of the formal “excluded amount” exceptions under the Tax on Split Income (TOSI) rules.

While the Excluded Business (20-hour active involvement test) is often the primary tool for small business owner-managers, the Reasonable Return Test becomes extremely important in situations involving:

- 💵 Capital contributions

- 🏢 Property contributed to the corporation

- ✍ Loan guarantees

- 📊 Partial involvement in the business

- 👩💼 Spouses who support the business financially but not full-time

If structured and documented properly, dividends paid under this test can avoid TOSI and be taxed normally.

Let’s break this down carefully and practically.

🧾 Step One: Age Categories Change the Rules

Under TOSI, the rules differ depending on age at year-end. The Canada Revenue Agency separates shareholders into:

- 👶 0–17 years old

- 🎓 18–24 years old

- 🧑 25 years and older

The Reasonable Return Test applies very differently depending on which category the shareholder falls into.

👶 Ages 0–17: No Access to the Reasonable Return Test

For minors:

❌ The kiddie tax rules apply

❌ Dividends are taxed at the highest marginal rate

❌ No reasonable return calculation is permitted

There is no flexibility here.

🎓 Ages 18–24: Restricted Reasonable Return (Prescribed Rate Model)

For individuals aged 18 to 24, the government assumes limited independent capital and imposes strict limits.

Here, the reasonable return is generally limited to:

- A return on arm’s length capital actually contributed

- Calculated using the prescribed rate

- No use of borrowed funds

- Strict tracing of capital

This is highly mechanical and restrictive.

📌 Example – 20-Year-Old Contributes Capital

Suppose:

- A 20-year-old contributes $50,000 of their own savings.

- The prescribed rate is 5%.

Reasonable return = $50,000 × 5% = $2,500.

A dividend around $2,500 may qualify.

A dividend of $25,000 likely would not.

The legislation is intentionally conservative for this age group.

🧑 Age 25 and Over: Broader, Flexible Logic Test

Once a shareholder is 25 or older at year-end, the analysis becomes more nuanced and flexible.

Now the test becomes:

🧠 Is the dividend reasonable based on the individual’s total contributions to the business?

This is sometimes called the “logic test.”

🔎 What Counts as a Contribution?

For individuals 25 and older, the following factors may support a reasonable return:

💰 Capital Contributed

- Cash invested at incorporation

- Share subscriptions

- Loans advanced

- Capital injections

- Reinvested dividends

Example:

If a spouse invested $200,000 at incorporation and receives a $10,000 dividend (5%), that may be reasonable.

🏢 Property Contributed

- Real estate used by the corporation

- Equipment or machinery

- Intellectual property

- Vehicles or tools

If a shareholder contributed a building used by the corporation, that is a meaningful economic contribution.

👷 Work Performed (Even Under 20 Hours)

Unlike the Excluded Business Test:

- The 20-hour bright-line rule does not apply here.

- Even 8–10 hours per week may count.

- Strategic or advisory involvement may count.

If a spouse handles marketing, vendor negotiations, compliance oversight, or administrative review, that work may support a reasonable return.

⚠ Risk Assumed

This is often overlooked but powerful.

Examples include:

- Personally guaranteeing bank loans

- Co-signing financing agreements

- Pledging personal assets as collateral

If a spouse guarantees a $500,000 operating line of credit, that is substantial economic risk.

That risk supports dividend payments.

📜 Historical Contributions

Past involvement and capital contributions can matter.

If a shareholder:

- Previously worked extensively

- Previously injected capital

- Previously guaranteed debt

Those historical factors may justify ongoing reasonable returns.

📊 Age Comparison Table

| Factor | Ages 18–24 | Age 25+ |

|---|---|---|

| Capital Contribution | Yes (strict) | Yes |

| Prescribed Rate Formula | Yes | No |

| Labour Contribution | Very limited | Yes |

| Risk Assumed | Limited | Yes |

| Subjective Case-by-Case Analysis | Limited | Yes |

🧠 What Does “Reasonable” Actually Mean?

There is no fixed percentage for those 25 and older.

Instead, the CRA evaluates:

- Industry norms

- Comparable market returns

- Size of capital invested

- Level of risk

- Nature of business

- Economic substance

The key professional question becomes:

Would an unrelated investor receive a similar return?

If yes, your position strengthens.

If no, TOSI risk increases.

📌 Practical Examples

✅ Scenario 1 – Moderate Return on Capital

- Invested: $300,000

- Dividend: $15,000

5% return.

Likely commercially defensible.

⚠ Scenario 2 – Minimal Contribution, Large Dividend

- Invested: $100

- Dividend: $40,000

Very difficult to defend as reasonable.

✅ Scenario 3 – Loan Guarantee + Partial Involvement

- No large capital injection

- Guaranteed major loan

- Works 10 hours per week

- Receives moderate dividend

Combined risk + involvement may support a reasonable return.

📂 Documentation Checklist

If relying on this test, documentation is critical.

Maintain:

✔ Share subscription agreements

✔ Loan agreements

✔ Property transfer documentation

✔ Loan guarantee contracts

✔ Financial statements

✔ Historical dividend records

✔ Capital contribution ledgers

✔ Board minutes referencing capital and risk

Without documentation, the argument weakens significantly.

⚖ Difference Between Active Involvement and Reasonable Return

| Active Involvement Test | Reasonable Return Test |

|---|---|

| Mechanical (20 hours/week) | Analytical & subjective |

| Bright-line threshold | Case-by-case evaluation |

| Focus on labour | Focus on capital, risk, labour |

| Most common | Secondary but powerful |

The reasonable return test is more flexible — but also more judgment-based.

🎯 When Should You Use This Test?

Use this test when:

- The shareholder does not meet the 20-hour rule

- There was meaningful capital contribution

- Significant financial risk was assumed

- Dividends reflect modest commercial returns

Avoid using it to justify aggressive income splitting.

📦 Professional Insight

In practice, for small owner-managed corporations:

- The Excluded Business Test will usually be your first approach.

- The Reasonable Return Test becomes valuable in spousal capital structures.

- It is particularly useful where one spouse funds the business but does not work full-time.

🏁 Final Takeaway

The Reasonable Return Test allows dividends to escape TOSI if they reflect genuine economic contributions.

Remember:

🔹 Ages 18–24 → Strict prescribed-rate limits

🔹 Age 25+ → Broader economic analysis

🔹 Must reflect real capital, labour, or risk

🔹 Documentation is essential

🔹 Dividend must be commercially defensible

This test requires professional judgment, economic reasoning, and careful documentation — but when applied correctly, it becomes a powerful tool in dividend planning under modern TOSI rules.

🏢 Excluded Shares Test for Non-Service Related Business Corporations

The Excluded Shares Test is one of the most technical — and often misunderstood — exceptions under the Tax on Split Income (TOSI) rules administered by the Canada Revenue Agency.

For a beginner tax preparer, here is the key takeaway right from the start:

⚠️ This exclusion is narrow.

⚠️ It does NOT apply to most professional corporations.

⚠️ It does NOT apply to most service-based businesses.

⚠️ It requires strict ownership and structural conditions.

This section will give you a complete, structured understanding so you can confidently analyze whether a client qualifies.

📘 What Is the Excluded Shares Test?

Under TOSI legislation, dividends received by certain individuals will not be subject to TOSI if those dividends are paid on shares that qualify as “excluded shares.”

If shares qualify:

✔ Dividends are taxed at normal marginal rates

✔ TOSI does not apply

✔ No highest-rate penalty taxation

However, all conditions must be satisfied.

🧾 Step 1: Age Requirement (25 or Older)

The shareholder must be:

- 🧑 25 years of age or older at the end of the taxation year.

If the individual is between 18–24 years old:

❌ The excluded shares test is unavailable.

They must instead rely on the reasonable return test (with prescribed rate limitations).

🗳 Step 2: Ownership Threshold — 10% Vote AND 10% Value

The shareholder must own:

- At least 10% of the voting shares, AND

- At least 10% of the fair market value of all issued shares.

Both requirements must be met.

⚠ Important Clarifications:

- Non-voting shares alone will not qualify.

- Owning 10% voting but only 5% value will not qualify.

- Preferred shares without voting rights generally fail.

This requirement forces genuine equity ownership — not token share issuance.

🚫 Step 3: Professional Corporations Are Excluded

This is one of the most critical restrictions.

The excluded shares test does NOT apply to:

- ❌ Law firms

- ❌ Accounting firms

- ❌ Dental corporations

- ❌ Medical corporations

- ❌ Other regulated professional corporations

Even if the spouse owns 50%, even if over 25, even if fully voting — this exclusion is unavailable.

Professional corporations were specifically carved out of this exception.

🏗 Step 4: The 90% Services Income Restriction

The corporation must not earn:

❗ 90% or more of its income from the provision of services.

If 90% or more of revenue is service income → excluded shares fail.

📌 What Is Considered “Service Income”?

Common examples:

- Consulting businesses

- IT contractors

- Personal service corporations

- Marketing agencies

- Engineering firms

- Financial advisors

- Freelance professionals

If the business primarily provides labour, expertise, or time — it is likely a service business.

📊 Quick Qualification Overview

| Requirement | Must Be Met? |

|---|---|

| Shareholder 25+ | ✅ Yes |

| Own ≥10% votes | ✅ Yes |

| Own ≥10% value | ✅ Yes |

| Not a professional corporation | ✅ Yes |

| Not 90%+ services income | ✅ Yes |

If any requirement fails → excluded shares do not apply.

🏢 Step 5: Related Business & Holding Company Complications

This is where complexity increases.

Consider this structure:

Operating Company → pays dividends → Holding Company → pays dividends → family shareholder

If the holding company’s income is derived from a related business, the excluded shares test may fail.

The legislation attempts to prevent:

- Dividend cascades

- Holdco income splitting

- Related-business flow-through planning

So if the dividend ultimately comes from a related operating business, TOSI risk remains.

🧠 Why This Rule Exists

The government introduced TOSI reforms to stop:

- Dividend sprinkling in service businesses

- Income splitting in professional corporations

- Passive holding company dividend chains

- Family members receiving dividends without real economic contribution

The excluded shares test was designed to protect:

- Genuine equity participation

- Non-service businesses

- Manufacturing and goods-producing corporations

It was not designed to preserve income splitting in professional or service contexts.

📦 Example 1 – Manufacturing Corporation (Possible Qualification)

Facts:

- Corporation manufactures furniture.

- 100% income from sale of goods.

- Spouse owns 20% voting common shares.

- Spouse owns 20% fair market value.

- Spouse is 40 years old.

✔ Age requirement met

✔ 10% vote requirement met

✔ 10% value requirement met

✔ Not professional

✔ Not service income

✅ Excluded shares likely apply.

Dividends may escape TOSI.

⚖ Example 2 – Consulting Business (Fails Services Test)

Facts:

- IT consulting corporation.

- 95% income from consulting services.

- Spouse owns 15% voting shares.

- Age 38.

❌ 90% services income restriction triggered.

Excluded shares unavailable.

Must rely on active involvement or reasonable return instead.

🏥 Example 3 – Professional Corporation (Fails Automatically)

Facts:

- Dental professional corporation.

- Spouse owns 25%.

- Age 50.

❌ Professional corporation exclusion.

The excluded shares test does not apply.

🏢 Example 4 – Holding Company Structure

Facts:

- Operating company earns active business income.

- Pays dividends to holding company.

- Holding company pays dividends to adult child.

Because income originates from a related operating business:

⚠ Excluded shares may not apply.

⚠ TOSI analysis required at individual level.

Holding companies do not automatically fix TOSI.

📂 Documentation Checklist for Practitioners

If attempting to rely on excluded shares, review:

✔ Articles of incorporation

✔ Share structure (classes & voting rights)

✔ Share register

✔ Ownership percentages

✔ Revenue breakdown (services vs goods)

✔ Corporate group structure

✔ Holding company relationships

Never assume eligibility without structural review.

🔍 Practical Reality for Most Small Businesses

In real-world small business practice:

- Most professional corporations will not qualify.

- Most consulting/service businesses will not qualify.

- Many holding company structures will not qualify.

- Manufacturing and goods-based companies may qualify.

This is why, practically, most owner-managers rely more heavily on:

1️⃣ Excluded Business (20-hour active involvement test)

2️⃣ Reasonable Return Test

The excluded shares test is secondary — and highly limited.

⚠ Why This Rule Is Confusing

This exclusion is complex because it combines:

- Age requirements

- Ownership thresholds

- Industry classification rules

- Professional carve-outs

- Related business analysis

- Holding company considerations

It is structural, not operational.

You must analyze corporate design — not just dividend payment.

🎯 Final Professional Takeaway

The Excluded Shares Test is:

🔹 Age restricted (25+)

🔹 Ownership-based (10% vote & value)

🔹 Not available for professional corporations

🔹 Not available for primarily service businesses

🔹 Complicated in holding company structures

It was intentionally drafted narrowly.

As a new tax preparer, your approach should be:

1️⃣ First test Active Involvement (20-hour rule).

2️⃣ Then analyze Reasonable Return.

3️⃣ Only then consider Excluded Shares — carefully and structurally.

If the ownership structure looks designed primarily to split income, TOSI risk is high.

Understanding this hierarchy will make you far more confident when advising owner-managed corporations under modern dividend rules.

📜 Letter to Lawyer to Update the Minute Book (Dividend Declaration Guide)

When dividends are declared in a corporation, it is not enough to simply record them in the accounting software or report them on the T2 return.

Dividends must be:

- ✅ Properly declared by directors

- ✅ Legally documented

- ✅ Recorded in the corporate minute book

- ✅ Reflected in resolutions

- ✅ Supported by share calculations

If this step is skipped, the dividend may be legally defective, even if tax was reported correctly.

As a tax preparer, this is where you move from “tax technician” to “corporate advisor.”

Let’s walk through this properly and practically.

⚖ Why the Minute Book Must Be Updated

When a corporation declares dividends:

- The directors must formally declare them.

- The declaration must specify the class of shares.

- The amount must be determined on a per-share basis.

- The payment date must be recorded.

- The resolution must be added to the minute book.

Without this documentation:

⚠ The dividend may not be legally enforceable.

⚠ Lawyers may flag deficiencies later during reorganizations.

⚠ Buyers may question validity in due diligence.

⚠ CRA may question corporate compliance.

This is why year-end dividend letters to lawyers are essential.

🗂 What the Year-End Letter to the Lawyer Accomplishes

Your letter:

1️⃣ Confirms the dividends declared

2️⃣ Provides exact per-share calculations

3️⃣ Specifies declaration and payment dates

4️⃣ Identifies share classes involved

5️⃣ Supplies totals for resolution drafting

6️⃣ Ensures the minute book is legally updated

You are giving the lawyer everything needed to draft:

- Director’s resolution

- Shareholder resolution (if required)

- Dividend register entry

📅 Important Dates to Include

The letter must clearly specify:

- 📆 Corporate year-end date

- 📆 Date dividends were declared

- 📆 Date dividends were paid

- 📆 Date financial statements were finalized (optional but helpful)

💡 Practical Tip:

Many practitioners declare dividends a few days before year-end and pay a few days later — rather than declaring and paying on December 31.

Example:

- Declared: December 27

- Paid: December 29

Is this mandatory? No.

But it adds clarity and corporate formality.

📊 Per-Share Calculations Are Mandatory

Dividends must be declared per share, not simply as a lump sum.

If a corporation has:

- 73,661 Class A shares outstanding

- Dividend per share: $0.695

Then:

Total dividend = 73,661 × 0.695 = $51,194.40

This is the number that must appear in the resolution.

🏢 Sample Breakdown Format for Lawyer Letter

Below is a structured format you can use in your letter.

🔹 Corporation Year-End

December 31, 20XX

🔹 Dividends Declared

Declared on: December 27, 20XX

Paid on: December 29, 20XX

🔹 Dividend Details by Share Class

| Share Class | Shares Outstanding | Dividend Per Share | Total Dividend |

|---|---|---|---|

| Class A | 73,661 | $0.695 | $51,194.40 |

If multiple classes exist, repeat the breakdown:

| Share Class | Shares Outstanding | Dividend Per Share | Total Dividend |

|---|---|---|---|

| Class B | 10,000 | $1.25 | $12,500 |

Each class must be calculated separately.

🧮 Why Per-Share Detail Matters

Dividends are declared at the class level.

You cannot:

❌ Arbitrarily allocate different amounts to shareholders of the same class.

❌ Declare $100,000 and split it unevenly if they hold identical shares.

The calculation must respect:

- Number of issued and outstanding shares

- Share class rights

- Articles of incorporation

This protects legal integrity.

📑 Eligible vs Ineligible Dividends

Your letter should also clarify whether dividends are:

- 🔵 Eligible dividends

- 🟢 Non-eligible (ineligible) dividends

This matters for:

- T5 preparation

- Personal tax reporting

- Corporate GRIP balance

- Lawyer’s resolution wording

Make sure classification is correct before issuing instructions.

✍ What the Lawyer Does With Your Letter

Once received, the lawyer will:

1️⃣ Draft director resolution declaring dividend

2️⃣ Record per-share amount

3️⃣ Record payment date

4️⃣ Insert documentation into minute book

5️⃣ Update corporate registers

You are not drafting the legal resolution — you are supplying the numerical and tax details.

🛑 Common Mistakes to Avoid

❌ Forgetting to specify declaration date

❌ Forgetting payment date

❌ Not calculating per-share amount

❌ Using rounded totals that don’t tie

❌ Ignoring share class distinctions

❌ Failing to confirm shares outstanding

❌ Declaring dividends when retained earnings insufficient

Always verify share count before sending instructions.

📂 Documentation Checklist Before Sending Letter

✔ Confirm share register

✔ Confirm issued & outstanding shares

✔ Confirm share classes

✔ Confirm dividend classification

✔ Confirm sufficient retained earnings

✔ Confirm declaration date

✔ Confirm payment date

✔ Recalculate totals

Never rely on memory or assumptions.

🧠 Why This Is So Important for You as a Tax Preparer

When preparing year-end corporate files:

- You are often the first person to determine dividend amounts.

- The lawyer relies on your accuracy.

- Errors can create legal defects.

If the minute book is not updated:

- Corporate reorganizations become messy.

- Future estate freezes become complicated.

- Purchasers may request corrective resolutions.

- Additional legal fees may arise.

Your letter prevents these issues.

🏗 Example Full Instruction Summary (Simplified Format)

Please update the minute book of ABC Corp. to reflect the following dividend declaration:

Corporate Year-End: December 31, 20XX

Dividends declared on December 27, 20XX

Dividends payable on December 29, 20XXClass A Shares:

- 73,661 shares issued and outstanding

- Dividend declared: $0.695 per share

- Total dividend: $51,194.40

- Dividend type: Non-eligible

That is sufficient for the lawyer to prepare proper documentation.

📌 Final Professional Takeaway

Declaring dividends involves three layers:

1️⃣ Tax reporting (T2 and T5)

2️⃣ Accounting entries

3️⃣ Legal documentation in the minute book

All three must align.

As a tax preparer, your responsibility includes ensuring:

- Accurate per-share calculations

- Clear declaration dates

- Proper communication with legal counsel

- Clean corporate documentation

This simple letter prevents future corporate headaches.

If you build the habit of preparing structured, detailed dividend instruction letters every year, you will:

✔ Protect your client

✔ Protect yourself

✔ Maintain corporate integrity

✔ Avoid legal cleanup work later

And that is what separates basic compliance from professional practice.

⚖️ Can Accountants Do the Minute Book Update as Part of Their Practice?

This is one of the most common questions new practitioners ask:

🧐 “Can I update a client’s minute book myself?”

🧐 “Is it required every year?”

🧐 “Do I need a lawyer involved?”

If you’re becoming a tax preparer, this is an important professional boundary question — not just a technical one.

Let’s break this down clearly from:

- 📚 Legal perspective

- 🧾 Practical reality

- 🏢 Risk management angle

- 🧠 Professional judgment standpoint

📘 First: What Is a Corporate Minute Book?

A corporate minute book is a legal record containing:

- Articles of incorporation

- Share registers

- Director registers

- Shareholder registers

- Annual shareholder minutes

- Director resolutions

- Dividend declarations

- Bonus approvals

- Share issuances

- Corporate changes

It is not an accounting file.

It is a legal document repository.

⚖️ The Technical Legal Answer

From a strict legal standpoint:

✅ Yes — the minute book must be updated annually.

✅ Yes — dividend declarations must be recorded.

✅ Yes — director resolutions must be documented.

Failure to update it means the corporation is not technically compliant with corporate law requirements.

So legally?

✔ It must be updated.

✔ Dividends must be declared properly.

✔ Resolutions must be recorded.

🏢 What Happens in Real-World Small Business Practice?

Here’s the reality in small owner-managed businesses:

- Many clients don’t know where their minute book is.

- Some have lost it.

- Many have not updated it in years.

- Most only update it when forced to.

When does it usually get updated?

🔎 When CRA audits

🔎 When shares are sold

🔎 When estate planning occurs

🔎 When there is a shareholder dispute

🔎 When the company is sold

Otherwise?

It often sits untouched.

🔍 Who Actually Looks at the Minute Book?

When the Canada Revenue Agency audits a corporation, one of the first requests is:

“Please provide the corporate minute book.”

Why?

They want to confirm:

- Who the directors are

- Who the shareholders are

- Who controls the corporation

- Who may be liable for GST/HST

- Who may be liable for payroll source deductions

They usually do not scrutinize every dividend resolution in detail.

But if something is missing, it can become an issue.

🧠 So… Can Accountants Update It?

This is where things become nuanced.

Technically:

Yes — accountants can draft resolutions.

But…

⚠️ Minute books contain legal documents.

⚠️ Lawyers are licensed to prepare legal documents.

⚠️ Professional accounting bodies often discourage preparing legal documents.